In The Upstart Startup, I highlighted that regulatory relief, in part, contributed to the exuberance surrounding the flood of investments in optical fiber construction during the late 1990s and early 2000s.

Cerent was born out of this change in supervisory oversight. It became the only manufacturing startup to capture billions of dollars in orders (for Cisco, as it later turned out) during the optical transport network builds serving the hearts of American cities.

Jeff Santos, one of Cerent’s three sales directors and marketer at heart, in our 2013 interview for my book, recalls the telecom market and the associated Telecommunications Act of 1996:

“There were things going on in the market where optical was certainly getting sexy because everybody needed bandwidth. It was all about optical, and the Telecom Act was hot and heavy and 10 years after the Telecom Act there was all of this glass in the ground that everybody was trying to exploit. Everybody was getting money from everywhere just because of how loose the financial space was back then. There were a lot of different characteristics of what was going on in the market, and not all of them healthy, by the way . . . Those were all of the dynamics that were leading towards the perfect storm.”

Money was easy to come by and venture capitalists were eager to fund both emerging service providers and startup equipment manufacturers. I wrote in The Upstart Startup:

“The year 1998 signaled the release of a flood of capital investment to build more facilities-based CLEC [Competitive Local Exchange Company] networks resembling Brooks Fiber Properties’ network. This frenzy forced many of these startup service providers to assume an inordinate amount of high-interest debt. Active venture capital firms investing in these new CLECs included Battery Partners, Crescendo Ventures, Crosspoint Ventures, Columbia Capital, Spectrum Equity Partners, and M/C Venture Partners. Unlike the modest investment of $7 million by NVP [Norwest Venture Partners] over a three-year period in Brooks Fiber Properties, typical investment rounds ballooned to about $100 million. Conventional wisdom held that the use of new technology underpinning these new service providers would enable the CLECs to beat the Baby Bells on price, just like MCI, Sprint, and Worldcom had done to AT&T in the long distance market years earlier. It was expected that the CLECs would quickly steal market share from incumbent telephone companies, a market worth some $100 billion.”

Cerent was born out of this change in supervisory oversight. It became the only manufacturing startup to capture billions of dollars in orders (for Cisco, as it later turned out) during the optical transport network builds serving the hearts of American cities.

Jeff Santos, one of Cerent’s three sales directors and marketer at heart, in our 2013 interview for my book, recalls the telecom market and the associated Telecommunications Act of 1996:

“There were things going on in the market where optical was certainly getting sexy because everybody needed bandwidth. It was all about optical, and the Telecom Act was hot and heavy and 10 years after the Telecom Act there was all of this glass in the ground that everybody was trying to exploit. Everybody was getting money from everywhere just because of how loose the financial space was back then. There were a lot of different characteristics of what was going on in the market, and not all of them healthy, by the way . . . Those were all of the dynamics that were leading towards the perfect storm.”

Money was easy to come by and venture capitalists were eager to fund both emerging service providers and startup equipment manufacturers. I wrote in The Upstart Startup:

“The year 1998 signaled the release of a flood of capital investment to build more facilities-based CLEC [Competitive Local Exchange Company] networks resembling Brooks Fiber Properties’ network. This frenzy forced many of these startup service providers to assume an inordinate amount of high-interest debt. Active venture capital firms investing in these new CLECs included Battery Partners, Crescendo Ventures, Crosspoint Ventures, Columbia Capital, Spectrum Equity Partners, and M/C Venture Partners. Unlike the modest investment of $7 million by NVP [Norwest Venture Partners] over a three-year period in Brooks Fiber Properties, typical investment rounds ballooned to about $100 million. Conventional wisdom held that the use of new technology underpinning these new service providers would enable the CLECs to beat the Baby Bells on price, just like MCI, Sprint, and Worldcom had done to AT&T in the long distance market years earlier. It was expected that the CLECs would quickly steal market share from incumbent telephone companies, a market worth some $100 billion.”

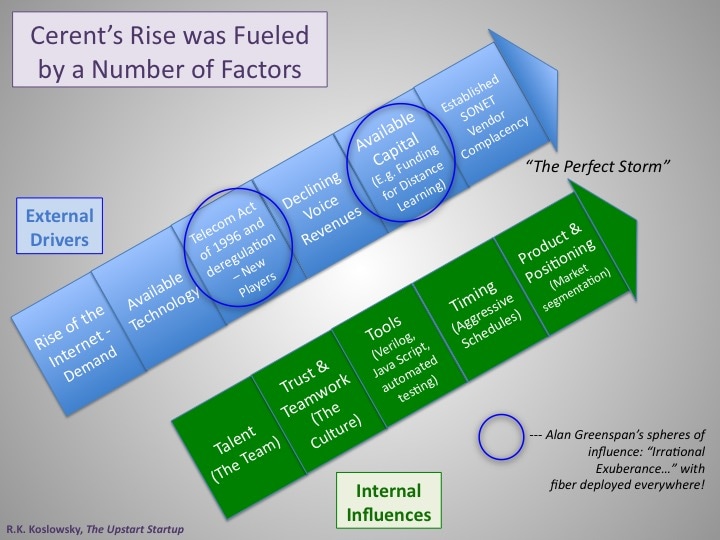

Alan Greenspan’s spheres of influence during the late 1990s. Graphic courtesy R.K. Koslowsky, copyright 2014.

Alan Greenspan, courtesy Bureau of Engraving and Printing, Federal Reserve

Alan Greenspan, courtesy Bureau of Engraving and Printing, Federal Reserve

Rana Foroohar, in her October 2016 column, found in TIME, observed, “[Alan] Greenspan, far from being a blind follower of ‘markets know best’ efficiency theory, was well aware that easy monetary policy and soaring stock prices could create bubbles – terribly damaging ones. And yet throughout his tenure, he allowed them to expand, believing them preferable to dramatic government interference in markets.”

Rana Foroohar, in her October 2016 column, found in TIME, observed, “[Alan] Greenspan, far from being a blind follower of ‘markets know best’ efficiency theory, was well aware that easy monetary policy and soaring stock prices could create bubbles – terribly damaging ones. And yet throughout his tenure, he allowed them to expand, believing them preferable to dramatic government interference in markets.”

But academics dispute this ongoing assertion made by mainstream media. Couper, Hejkal, and Wolman, in the fall of 2003, argued, “With the benefit of hindsight, most people would say that telecommunications stocks were overvalued at their peak, and that too much investment took place in the telecommunications sector in the late 1990s. However, any time there is great uncertainty or rapid change in a market environment, one should not be surprised, ex post, to observe large forecast errors.”

They conclude, “Thus, our explanation for the telecommunications boom and bust does not involve fraud, irrationality, or a bubble. To be sure, as the bust became apparent [in 2002], fraud did occur. But it is not clear that fraud played an important role in the boom and the early stages of the bust . . . We see the boom and bust as—in large part—a rational response to the changing fundamentals of technology and regulatory environment.”

Jeff Santos, wryly observed, “Most everybody we ever sold to was either acquired or going out of business.”

Irrational Exuberance

Investment hysteria took over during the late 1990s. Money rolled into the coffers of the CLECs anxious to build a new broadband infrastructure in the metropolitan networks and beyond. Thomson Financial data reveals that funding in the U.S. for CLECs mushroomed to $4.25 billion in 1999 and peaked at $6.7 billion the following year. Big returns were expected, but unknown to many and ignored by numerous industry insiders, was the fact that most CLECs had taken on too much debt, too quickly. Interest payments on the money they raised often outstripped the revenue taken in. Many CLECs would not survive, nor would many equipment manufacturers . . . but the foundation of telecom networks would change forever, as fiber replaced copper connections and packet replaced circuit switching.

It was a time that tested one’s spirit. As Charles Dickens opened in A Tale of Two Cities, “It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity . . . ”

Indeed, the 1990s were all of this, and more.

This period of massive overinvestment in the telecom sector, and in deployment of optical fiber cable around the country, led to the telecom meltdown. Couper et al succinctly described the situation: “Stock prices plunged and investment collapsed. These problems were exacerbated by the U.S. economy’s swing into recession early in 2001, and the telecommunications sector remains in a slump to this day.” [1]

But there is a silver lining, and all startups, both from the service offerings side and the technology investment side, should be recognized for this success [2]. The interaction of regulatory relief and technological advancement ultimately delivered significantly lower consumer prices for existing services and a new menu of advanced services.

[1] “To this day” refers to the autumn of 2003, but one can argue that the telecom slump remains through 2016. If Cisco’s stock is a barometer of the telecommunications market, then that company’s $80 stock price from the Greenspan era, has never even regained half its value to reach $40 per share.

[2] Couper, Hejkal, and Wolman wrote, “. . . advances in basic technology for providing telecommunications services would have two implications. First, because the capacity of existing networks would increase dramatically, the price of existing services would be expected to fall. Second, the increase in capacity, and in speed, would lead to the development of new applications which benefited from high-speed, high-capacity [optical fiber] transmission. To cite one example that has already been observed, the World Wide Web is a telecommunications application which relied on relatively high-speed modems for its practicality. Looking ahead, high-quality streaming video is an application that relies on data transfer speeds greater than are currently available. The interaction between basic technology (speed and capacity) and new applications represents a virtuous circle in which new applications lead to demand for bandwidth, and demand for bandwidth provides the impetus for new supply of bandwidth, which in turn makes new, bandwidth-hungry applications feasible. To a large extent, belief in the relevance of this interaction fueled the telecommunications boom.” The Cerent 454 provided the speed and capacity to support simultaneous carriage of voice, data, and video, which supported the telecom boom.

They conclude, “Thus, our explanation for the telecommunications boom and bust does not involve fraud, irrationality, or a bubble. To be sure, as the bust became apparent [in 2002], fraud did occur. But it is not clear that fraud played an important role in the boom and the early stages of the bust . . . We see the boom and bust as—in large part—a rational response to the changing fundamentals of technology and regulatory environment.”

Jeff Santos, wryly observed, “Most everybody we ever sold to was either acquired or going out of business.”

Irrational Exuberance

Investment hysteria took over during the late 1990s. Money rolled into the coffers of the CLECs anxious to build a new broadband infrastructure in the metropolitan networks and beyond. Thomson Financial data reveals that funding in the U.S. for CLECs mushroomed to $4.25 billion in 1999 and peaked at $6.7 billion the following year. Big returns were expected, but unknown to many and ignored by numerous industry insiders, was the fact that most CLECs had taken on too much debt, too quickly. Interest payments on the money they raised often outstripped the revenue taken in. Many CLECs would not survive, nor would many equipment manufacturers . . . but the foundation of telecom networks would change forever, as fiber replaced copper connections and packet replaced circuit switching.

It was a time that tested one’s spirit. As Charles Dickens opened in A Tale of Two Cities, “It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity . . . ”

Indeed, the 1990s were all of this, and more.

This period of massive overinvestment in the telecom sector, and in deployment of optical fiber cable around the country, led to the telecom meltdown. Couper et al succinctly described the situation: “Stock prices plunged and investment collapsed. These problems were exacerbated by the U.S. economy’s swing into recession early in 2001, and the telecommunications sector remains in a slump to this day.” [1]

But there is a silver lining, and all startups, both from the service offerings side and the technology investment side, should be recognized for this success [2]. The interaction of regulatory relief and technological advancement ultimately delivered significantly lower consumer prices for existing services and a new menu of advanced services.

[1] “To this day” refers to the autumn of 2003, but one can argue that the telecom slump remains through 2016. If Cisco’s stock is a barometer of the telecommunications market, then that company’s $80 stock price from the Greenspan era, has never even regained half its value to reach $40 per share.

[2] Couper, Hejkal, and Wolman wrote, “. . . advances in basic technology for providing telecommunications services would have two implications. First, because the capacity of existing networks would increase dramatically, the price of existing services would be expected to fall. Second, the increase in capacity, and in speed, would lead to the development of new applications which benefited from high-speed, high-capacity [optical fiber] transmission. To cite one example that has already been observed, the World Wide Web is a telecommunications application which relied on relatively high-speed modems for its practicality. Looking ahead, high-quality streaming video is an application that relies on data transfer speeds greater than are currently available. The interaction between basic technology (speed and capacity) and new applications represents a virtuous circle in which new applications lead to demand for bandwidth, and demand for bandwidth provides the impetus for new supply of bandwidth, which in turn makes new, bandwidth-hungry applications feasible. To a large extent, belief in the relevance of this interaction fueled the telecommunications boom.” The Cerent 454 provided the speed and capacity to support simultaneous carriage of voice, data, and video, which supported the telecom boom.

RSS Feed

RSS Feed