“I never heard that Carl [Russo] had his eye on Ciena . . . the CoreDirector, [a massive electrical (STS-1) switching platform], combined with the Cerent 454 would have exponentially annihilated the competition.”

- Tom Randstrom, former Cerent and Cisco employee

- Tom Randstrom, former Cerent and Cisco employee

Tom is one of many in the telecom business that had never heard about Carl Russo’s designs for startup Cerent to acquire Ciena for its long haul and high bandwidth electrical switching platforms during 1999. Here is what happened . . .

The setting: By March 1999, acquisitions for optical companies were being completed in the $500 to $600 million range. Ciena’s acquisition of Lightera in mid-March was no different. Ciena acquired all of Lightera in exchange for about 20.6 million Ciena common shares or about $552 million. The deal was expected to help Ciena establish itself as a credible alternative to Nortel and Lucent for the long-haul fiber-optic networks that local and long-distance phone companies were building at the time.

The reaction: Vinod Khosla was not happy with this development as he viewed Lightera as a complement to what Cerent was building across metropolitan networks.

The response after Cisco approached Cerent (to be acquired): Carl’s brain went into hyperdrive, especially after thinking about the Ciena acquisition of Lightera . . . Once Lightera’s STS-1 cross-connect functionality was removed from the market, Cerent’s technical positioning was undermined. As Carl recalls, “If we would have just stayed in the position we were in we were going to be in a seam, a big seam.”

But there was more to it than falling into a “death valley” where growth would be stymied in the long run. Carl and the Cerent board had considered not only solidifying the metropolitan transport space, but also expanding into the long-haul space that Nortel dominated [in the late 1990s]. Carl adds, “Our goal, as Cerent, was to acquire Ciena and to acquire whatever we needed to acquire because the view was that this market cap was going to last only as long as the market would last and you better fucking well use it. There’s no sense riding it up and riding it down.”

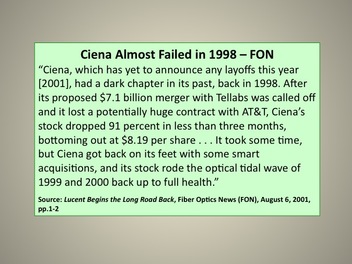

Cerent acquiring Ciena was doable at the time. Ciena’s falling stock price in late 1998 and most of 1999 opened up this avenue of “growth by acquisition” for Cerent. Ciena had missed some of its financial quarters and the company’s market cap had actually fallen to the $2.5 to $3.0 billion range. The share price fell from a high of $245 in June 1998 to $109 in June 1999, hitting lows in between of $44 per share in September 1998 and $52 per share in January 1999. Ciena's share price even briefly flitted with the single digits in 1998.

Carl adds, “And we likely could have gone public at greater than ten billion dollars. Our plan was to go after Ciena and by the way, if it had to be a hostile acquisition, make it hostile. We didn’t care.”

Indeed, Ciena’s market cap had fallen below Cerent’s expected valuation if the [startup] went public . . . Carl had his sights set. Ciena had good long-haul technology and they had Lightera, which was the STS-1 fabric switch. Carl’s plan was to get Ciena and recover the Lightera technology, but the intervening offer from Cisco shot down his strategy.

“I knew that we were done, in that microsecond,” Carl concludes, “and I was already in the mode of ‘I need to go extract the largest number I could from Cisco.’”

Oh, well: So an approach to grow organically by acquiring Ciena was thwarted during the summer of 1999. Cisco would not be denied access to optical technology it desperately needed. Quite simply put, a bigger fish ate a growing fish that was after a troubled fish in the telecom ocean of 1999.

The reaction: Vinod Khosla was not happy with this development as he viewed Lightera as a complement to what Cerent was building across metropolitan networks.

The response after Cisco approached Cerent (to be acquired): Carl’s brain went into hyperdrive, especially after thinking about the Ciena acquisition of Lightera . . . Once Lightera’s STS-1 cross-connect functionality was removed from the market, Cerent’s technical positioning was undermined. As Carl recalls, “If we would have just stayed in the position we were in we were going to be in a seam, a big seam.”

But there was more to it than falling into a “death valley” where growth would be stymied in the long run. Carl and the Cerent board had considered not only solidifying the metropolitan transport space, but also expanding into the long-haul space that Nortel dominated [in the late 1990s]. Carl adds, “Our goal, as Cerent, was to acquire Ciena and to acquire whatever we needed to acquire because the view was that this market cap was going to last only as long as the market would last and you better fucking well use it. There’s no sense riding it up and riding it down.”

Cerent acquiring Ciena was doable at the time. Ciena’s falling stock price in late 1998 and most of 1999 opened up this avenue of “growth by acquisition” for Cerent. Ciena had missed some of its financial quarters and the company’s market cap had actually fallen to the $2.5 to $3.0 billion range. The share price fell from a high of $245 in June 1998 to $109 in June 1999, hitting lows in between of $44 per share in September 1998 and $52 per share in January 1999. Ciena's share price even briefly flitted with the single digits in 1998.

Carl adds, “And we likely could have gone public at greater than ten billion dollars. Our plan was to go after Ciena and by the way, if it had to be a hostile acquisition, make it hostile. We didn’t care.”

Indeed, Ciena’s market cap had fallen below Cerent’s expected valuation if the [startup] went public . . . Carl had his sights set. Ciena had good long-haul technology and they had Lightera, which was the STS-1 fabric switch. Carl’s plan was to get Ciena and recover the Lightera technology, but the intervening offer from Cisco shot down his strategy.

“I knew that we were done, in that microsecond,” Carl concludes, “and I was already in the mode of ‘I need to go extract the largest number I could from Cisco.’”

Oh, well: So an approach to grow organically by acquiring Ciena was thwarted during the summer of 1999. Cisco would not be denied access to optical technology it desperately needed. Quite simply put, a bigger fish ate a growing fish that was after a troubled fish in the telecom ocean of 1999.

RSS Feed

RSS Feed