The Cerent team, with its popular Cerent 454 optical transport product, defined the “smart” category for optical fiber systems – the so-called Multi-service Provisioning Platform (MSPP) class. Most industry analysts embraced this differentiation for these emerging “next generation” SONET products from the legacy SONET products concocted a decade earlier.

One industry analyst firm, Infonetics Research, led by Michael Howard, preferred to use the term “intelligent optical network hardware.” Under their classification Infonetics reported, “Worldwide revenues for intelligent optical network hardware hit $11.4 billion in 2001, a 67 percent growth over 2000, and are projected to double to $23 billion in 2005.” [1]

One industry analyst firm, Infonetics Research, led by Michael Howard, preferred to use the term “intelligent optical network hardware.” Under their classification Infonetics reported, “Worldwide revenues for intelligent optical network hardware hit $11.4 billion in 2001, a 67 percent growth over 2000, and are projected to double to $23 billion in 2005.” [1]

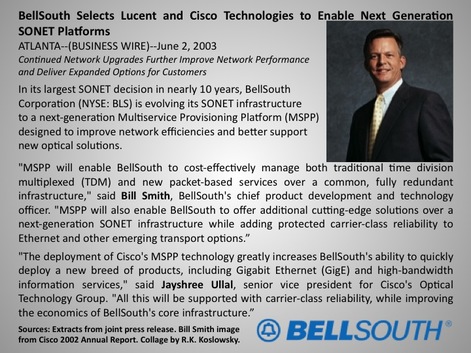

Cisco was the big winner in the BellSouth award for next generation optical transport equipment.

Cisco was the big winner in the BellSouth award for next generation optical transport equipment. Regardless of the category’s designation [2], the Cerent 454 (renamed the Cisco ONS 15454) did very well in the early 2000s, continuing to rack up major wins in the metropolitan market, such as the selection by BellSouth [3].

However, it’s baby brother, the ONS 15327, a scaled down ‘454,’ underperformed and came across as too telco-centric for the customer premise (or Enterprise) market and too high-priced to crack the optical transport market in a big way.

The subsequent optical switching product, the Cisco ONS 15600, came too late to the market and never really challenged the Ciena CoreDirector offering which rapidly became the #1 seller in its category.

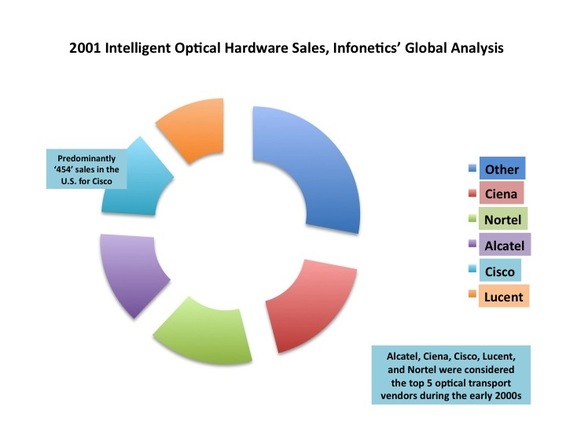

Five manufacturers accounted for 72 percent (or $9 billion) of the 2001 global revenue market for intelligent optical hardware. These numbers excluded submarine hardware. As reflected in the pie chart below, Ciena led at 18 percent, Cisco followed with 13 percent, based on pretty much just one product – the ‘454,’ and Lucent brought up the rear with an 11 percent share.

Five manufacturers accounted for 72 percent (or $9 billion) of the 2001 global revenue market for intelligent optical hardware. These numbers excluded submarine hardware. As reflected in the pie chart below, Ciena led at 18 percent, Cisco followed with 13 percent, based on pretty much just one product – the ‘454,’ and Lucent brought up the rear with an 11 percent share.

Data courtesy Infonetics; graphic by R.K. Koslowsky.

It just goes to show how a product can change the market it dominates without always being listed as #1 in every possible way the chosen data can be sliced.

[1] Fiber Optics News, Intelligent Optical Network Hardware Market Hits $11.4B in 2001, March 11, 2002, p.8.

[2] Infonetics’ definition, some three years after the fact, was simply another way of describing MSPP in the metro, the category previously defined by Cerent. However, Infonetics’ definition covered ALL market segments.

[3] Even though BellSouth listed Lucent first in this joint Press Release (PR), retaining Lucent as their “other” SONET vendor, Cisco was the big winner in this award for next generation optical transport equipment. About Lucent, the PR said, “BellSouth will utilize the Lucent Metropolis DMX Access Multiplexer that is currently being deployed for use in interoffice networks and end customer high bandwidth ring applications . . .”

Graphic courtesy R.K. Koslowsky

RSS Feed

RSS Feed