Mike Hatfield drove “Cerent’s” business plan, which culminated in a June 24, 1997 document outlining Fiberlane’s product strategy, competitive position, strategic partnerships, and target customers along with proposed financials. The plan called for company profitability by the third quarter of 1999, leading to an overall breakeven position. These were aggressive, but achievable goals, however, ones that no longer resonated with Wall Street’s expectations, which became based on revenue growth more so than achieving profitability. The rise of dot.com companies and the meteoric ascension of new telecom service providers oversaw incredible business growth. The new normal became “growth.”

Carl Russo perceived this change in the business environment as he joined the Fiberlane splinter renamed Cerent and replaced Mike as the leader. The direction that demanded Cerent reach a cash flow positive position and work off the debt and then finally reach an investment positive state was abandoned. This halt to Mike’s plan flew in the face of his common sense and previous AFC experience.

Paul Elliott and others on the Petaluma-based team, before Carl became CEO, subscribed to these “old school” business rules too, “Carl realized that things had changed. Growth was being valued, so any money we got, we’d invest in expansion.”

To worry about reaching profitability sooner rather than later was thrown out the window. What became more important to Carl was selling product and building the business along a growth trajectory. Growth, the latest be-all and end-all on Wall Street, meant that stock prices rose and company valuations increased. Growth became the quintessential element defining the success of a company.

Paul remembers, “Carl changed our priorities; our emphasis was no longer on becoming cash flow positive. The emphasis was on achieving some exponential growth curve.”

The consensus remains to this day that Carl grew Cerent much faster than Mike would have. It was a bold and risky strategy that Carl embraced. If things had gone wrong, they would have gone wrong in a big way and it was likely Cerent would not have recovered.

Carl Russo perceived this change in the business environment as he joined the Fiberlane splinter renamed Cerent and replaced Mike as the leader. The direction that demanded Cerent reach a cash flow positive position and work off the debt and then finally reach an investment positive state was abandoned. This halt to Mike’s plan flew in the face of his common sense and previous AFC experience.

Paul Elliott and others on the Petaluma-based team, before Carl became CEO, subscribed to these “old school” business rules too, “Carl realized that things had changed. Growth was being valued, so any money we got, we’d invest in expansion.”

To worry about reaching profitability sooner rather than later was thrown out the window. What became more important to Carl was selling product and building the business along a growth trajectory. Growth, the latest be-all and end-all on Wall Street, meant that stock prices rose and company valuations increased. Growth became the quintessential element defining the success of a company.

Paul remembers, “Carl changed our priorities; our emphasis was no longer on becoming cash flow positive. The emphasis was on achieving some exponential growth curve.”

The consensus remains to this day that Carl grew Cerent much faster than Mike would have. It was a bold and risky strategy that Carl embraced. If things had gone wrong, they would have gone wrong in a big way and it was likely Cerent would not have recovered.

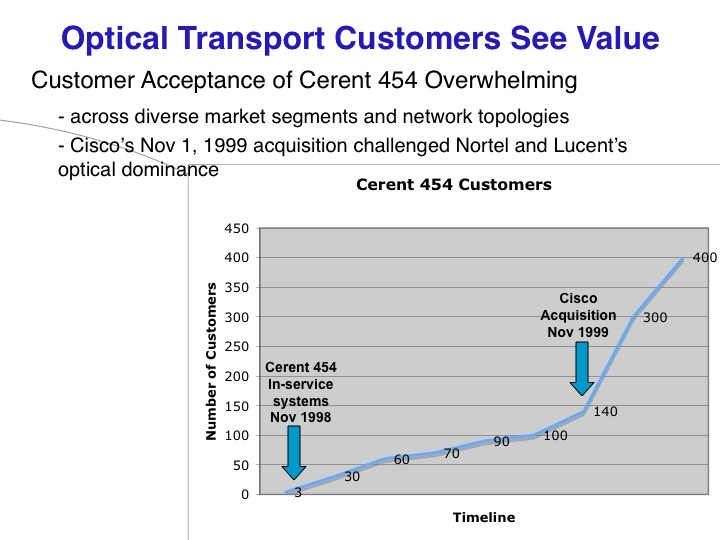

Carl invested heavily in sales and marketing and the result was a rapid uptake in customers during 1999 through 2001.

On the other hand, if Cerent had remained more bottom line-oriented, the company could have backed off in down times and coasted through a rough patch and kept on sailing through to the other side. However, Cerent would not have been prepared for the customer growth it did achieve. Even so, not even Carl could have predicted the exuberant demand for the Cerent 454 to come in the final months of the old millennium.

Carl recognized that growth was tied to valuation and he amped up the infrastructure to support both growing the organization and hence the ability to build more product as well as courting more investors. Cisco began to take notice too, ultimately valuing the company at $6.9 billion for the remaining 90 percent stake it did not own.

Looking back on this time, Mark Grinblatt, UCLA finance professor, said in 2000, "You need less of a so-called traditional business model [to go public] than you did in the past. You don't need to have earnings to have value. People are valuing these companies based on growth potential." But Carl had more than growth potential, he led a startup blessed with real growth fueled by many customers and repeated sales from a rapidly increasing customer base. He believed Cerent was worth a lot more than his fellow board members concluded.

Carl is a quick learner and a consummate actor. He came from a different industry and with it he brought the emphasis on getting things done quickly, just like he did in the computer industry. And at a startup, even at a telecom startup, things can be done quickly.

Paul observed, “It was just a perfect time to be doing what we were doing. The whole market was growing as we were growing. It was a golden moment.”

But all good things must come to an end. By 2002, the golden geese of the dot.com and telecom booms were no longer laying golden eggs. In part, companies that abandoned profitability and had very little revenues to show failed in record numbers. University of Florida Professor Jay Ritter, recently reported that in 1999 and 2000 only 14 and 13 percent of technology company IPOs, respectively, were profitable, down from the pre-dot.com era of 1996 and 1997, when 43 and 46 percent of them, respectively, were profitable.

Jay cautions that a similar situation is appearing today with only 11 percent of the technology IPOs from 2014 operating at a profit, a level even below the 13 percent of 2000.

Could there be another technology bust in the near future?

It seems a balance needs to be struck between growth and profitability for public companies to remain successful and avoid their own bust.

Carl recognized that growth was tied to valuation and he amped up the infrastructure to support both growing the organization and hence the ability to build more product as well as courting more investors. Cisco began to take notice too, ultimately valuing the company at $6.9 billion for the remaining 90 percent stake it did not own.

Looking back on this time, Mark Grinblatt, UCLA finance professor, said in 2000, "You need less of a so-called traditional business model [to go public] than you did in the past. You don't need to have earnings to have value. People are valuing these companies based on growth potential." But Carl had more than growth potential, he led a startup blessed with real growth fueled by many customers and repeated sales from a rapidly increasing customer base. He believed Cerent was worth a lot more than his fellow board members concluded.

Carl is a quick learner and a consummate actor. He came from a different industry and with it he brought the emphasis on getting things done quickly, just like he did in the computer industry. And at a startup, even at a telecom startup, things can be done quickly.

Paul observed, “It was just a perfect time to be doing what we were doing. The whole market was growing as we were growing. It was a golden moment.”

But all good things must come to an end. By 2002, the golden geese of the dot.com and telecom booms were no longer laying golden eggs. In part, companies that abandoned profitability and had very little revenues to show failed in record numbers. University of Florida Professor Jay Ritter, recently reported that in 1999 and 2000 only 14 and 13 percent of technology company IPOs, respectively, were profitable, down from the pre-dot.com era of 1996 and 1997, when 43 and 46 percent of them, respectively, were profitable.

Jay cautions that a similar situation is appearing today with only 11 percent of the technology IPOs from 2014 operating at a profit, a level even below the 13 percent of 2000.

Could there be another technology bust in the near future?

It seems a balance needs to be struck between growth and profitability for public companies to remain successful and avoid their own bust.

RSS Feed

RSS Feed