The shift from legacy SONET/SDH optical transport solutions to Multi-Service Provisioning Platforms (MSPP), pioneered by Cerent, accelerated at a greater rate as the year 2001 began.

Industry analyst, Frost & Sullivan, in their 2001 report, Traditional SONET/SDH Optical Networking Systems, highlighted that the optical transport industry “is rapidly yielding revenues to next generation systems. After producing revenues of $15.5 billion in 2000, this market will decline below $9.4 billion by 2005.”

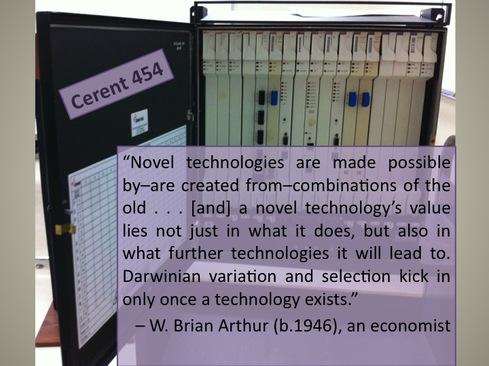

The Cerent 454, rebranded by Cisco as the ONS 15454, in 2000, delivered higher capacity for metro optical transport with its OC-192 option as well as the integrated DWDM options at both OC-48 and OC-192 bit rates. The integrated management platform for this gear, which brought intelligent A-to-Z provisioning capabilities, for example, reduced operational costs and made it easier for operators to use.

The Fiber Optics News story of August 2001 [1], reported, “‘More than 50 percent of all optical network spending went toward traditional optical equipment in 2000,’ says Mark Storm, Frost & Sullivan program leader. ‘The trend is clear that service providers will transition their purchasing pattern toward next-generation equipment as they migrate toward higher capacity, multi-wavelength, intelligent optical networking solutions.’”

Industry analyst, Frost & Sullivan, in their 2001 report, Traditional SONET/SDH Optical Networking Systems, highlighted that the optical transport industry “is rapidly yielding revenues to next generation systems. After producing revenues of $15.5 billion in 2000, this market will decline below $9.4 billion by 2005.”

The Cerent 454, rebranded by Cisco as the ONS 15454, in 2000, delivered higher capacity for metro optical transport with its OC-192 option as well as the integrated DWDM options at both OC-48 and OC-192 bit rates. The integrated management platform for this gear, which brought intelligent A-to-Z provisioning capabilities, for example, reduced operational costs and made it easier for operators to use.

The Fiber Optics News story of August 2001 [1], reported, “‘More than 50 percent of all optical network spending went toward traditional optical equipment in 2000,’ says Mark Storm, Frost & Sullivan program leader. ‘The trend is clear that service providers will transition their purchasing pattern toward next-generation equipment as they migrate toward higher capacity, multi-wavelength, intelligent optical networking solutions.’”

Image and collage courtesy R.K. Koslowsky

MSPPs became all the rage. The incumbent equipment vendors (Nortel, Lucent, Alcatel, and the like) fought tooth and nail to keep their large service provider customers focused on spending capital dollars on legacy SONET/SDH solutions, but they could not stop the Cerent momentum. Cerent had more than 120 customers from the Tier 3 and Tier 2 service provider segment before Cisco acquired the upstart startup. Then Cisco supported the Cerent team who rapidly reached 500-plus customers for the rebranded ‘454,’ including major Tier 1 suppliers such as AT&T, QWEST, U S WEST, BellSouth, SBC, and others.

“Vendors that do not adapt to rapid product cycles and embrace a distributed manufacturing model will perish,” said Storm, in his interview with Fiber Optics News. “However, vendors that prune their product mix and operations and embrace customer demand for multi-vendor network deployments will be very difficult to displace.”

Indeed. An initial reluctance to change to address the rise of the MSPP solution introduced by Cerent, adversely affected Lucent and Nortel the most. Cisco, on the other hand, adopted changed through its acquisition-and develop-strategy, which allowed it to enter the service provider market (with Cerent’s products and sales team) and organically grow. By 2015, Cisco’s service provider market segment provided at least one-third of its revenue stream.

And an even greater benefit to all of Cisco; the company ended up manufacturing more reliable and higher quality products across all of its product groups as the telco notions of five “9”s reliability and system testing found fertile ground within the Internet giant’s quality group and manufacturing partners.

And for the Cerent 454, it evolved from SONET technology, and after its productive run, set the stage for the next evolutionary stage that took the industry from MSPPs to ROADMs (Reconfigurable Optical Add-Drop Multiplexers) . . . and the beat goes on.

[1] Technological Darwinism Alters Optical Market, Fiber Optics News, August 6, 2001, p.1

“Vendors that do not adapt to rapid product cycles and embrace a distributed manufacturing model will perish,” said Storm, in his interview with Fiber Optics News. “However, vendors that prune their product mix and operations and embrace customer demand for multi-vendor network deployments will be very difficult to displace.”

Indeed. An initial reluctance to change to address the rise of the MSPP solution introduced by Cerent, adversely affected Lucent and Nortel the most. Cisco, on the other hand, adopted changed through its acquisition-and develop-strategy, which allowed it to enter the service provider market (with Cerent’s products and sales team) and organically grow. By 2015, Cisco’s service provider market segment provided at least one-third of its revenue stream.

And an even greater benefit to all of Cisco; the company ended up manufacturing more reliable and higher quality products across all of its product groups as the telco notions of five “9”s reliability and system testing found fertile ground within the Internet giant’s quality group and manufacturing partners.

And for the Cerent 454, it evolved from SONET technology, and after its productive run, set the stage for the next evolutionary stage that took the industry from MSPPs to ROADMs (Reconfigurable Optical Add-Drop Multiplexers) . . . and the beat goes on.

[1] Technological Darwinism Alters Optical Market, Fiber Optics News, August 6, 2001, p.1

RSS Feed

RSS Feed