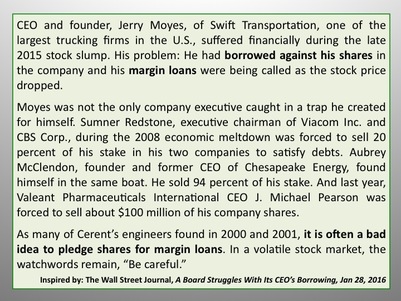

Startup Cerent was acquired by Cisco for $6.9 billion in late 1999. The financial arrangement produced more than 250 millionaires, most living in Sonoma County, California. But not all was coming up roses for many of these “lucky” individuals, most of whom were male engineers in their 30s and 40s. (Yes, it was a highly educated, upwardly mobile group of experienced individuals.)

But something happened to many of these young entrepreneurs who suddenly had millions of dollars at their disposal. Bob Bortolotto, one of Cerent’s hardware engineering leaders, believes the money many engineers made from Cerent being acquired hurt as many people as it helped: “For every story about someone that is happily retired there is another story of how the money destroyed a life. It had as much negative impact as positive impact.”

Bob recalled the danger of the “wealth effect” and how it affected many of the Cerent engineers, “The people that got creamed were those that made one million bucks or so. All of a sudden they became millionaires on paper and they didn’t know anything about capital gains taxes and the importance of investing and diversifying that amount of money. Many of the engineers in their naïveté just winged it and, as a result, boosted the local economy by purchasing some toys, fancy cars, and a new house. Then next April rolled around and they owed a quarter of a million or more in taxes and they didn’t have it.”

But something happened to many of these young entrepreneurs who suddenly had millions of dollars at their disposal. Bob Bortolotto, one of Cerent’s hardware engineering leaders, believes the money many engineers made from Cerent being acquired hurt as many people as it helped: “For every story about someone that is happily retired there is another story of how the money destroyed a life. It had as much negative impact as positive impact.”

Bob recalled the danger of the “wealth effect” and how it affected many of the Cerent engineers, “The people that got creamed were those that made one million bucks or so. All of a sudden they became millionaires on paper and they didn’t know anything about capital gains taxes and the importance of investing and diversifying that amount of money. Many of the engineers in their naïveté just winged it and, as a result, boosted the local economy by purchasing some toys, fancy cars, and a new house. Then next April rolled around and they owed a quarter of a million or more in taxes and they didn’t have it.”

Sale of stocks produced cash to buy homes, but the associated capital gains produced a tax bill that many could not pay the following year. Image courtesy Storify.

Meanwhile the stock market fell and any unvested Cisco stock was devalued. Engineers who were buying on margin in order to start the capital gains ticker saw this strategy fail. They entered into financial arrangements expecting the Cisco stock to continue to soar to new heights. However, as soon as the Cisco stock went down and stayed down, it was all over for them. It ruined them financially.

This trapped many engineers who had vested with a lot of money and then they needed to pay large tax bills in 1999 and 2000 and settle up on margin loan deals gone south. Bob recalls, “The power of money, what it did to them, how it changed their personality, it was scary. In a lot of ways it wasn’t a good thing.”

This trapped many engineers who had vested with a lot of money and then they needed to pay large tax bills in 1999 and 2000 and settle up on margin loan deals gone south. Bob recalls, “The power of money, what it did to them, how it changed their personality, it was scary. In a lot of ways it wasn’t a good thing.”

The tax man cometh. Sale of stocks produced cash which was quickly spent, with little saved to pay the looming tax bills in April of the following year. Image courtesy Storify.

The same lessons of 2000 and 2001 are being re-learned in 2015 and 2016 too.

The same lessons of 2000 and 2001 are being re-learned in 2015 and 2016 too. The same lessons were re-learned by many other people across America who had amassed money and invested in the stock market leading up to the 2007–2008 housing bubble burst and ensuing recession. They went “all in” for equities and ignored the lessons of diversification, hoping that another bear market was far off into the future.

In 1999, many people in the middle class made this mistake and invested in the equity markets exclusively; Cerent’s engineers included. They were overconfident that Wall Street’s big returns in a bull market that had existed since 1982 would continue well into the new millennium. During this eighteen-year period, the Dow experienced its most spectacular rise, although with a “minor blip” in 1987. From a low of 777 in August 1982, the index grew more than 1,500 percent to close at almost 11,723 by January 2000. Then the bear market arrived, which lasted until 2003. The index weaved and bobbed at first, like an ocean buoy, and then plunged nearly 40 percent, to a low of 7,286 in October 2002.

But the technology sector and Cisco’s stock price in particular had a far rougher ride and with it the engineers who kept everything or most of their paper wealth invested in Cisco after December 1999. Cisco’s stock price peaked in March 2000 at just over $80 per share and in nine months it lost more than half its value to around $39 per share. The stock took another 100 percent hit in less than three months, reaching a further low of just over $20 per share. Between March and September 2001, another halving of the stock price took place, with shares settling to a low under $12 share.

Anyone making a million dollars from vesting in or buying more Cisco stock saw their money effectively cut in half on three different occasions over an eighteen-month period. This turn of events left newly-minted Cisco millionaires with $125,000, a number that is found in numerous middle-aged, middle-class couples’ combined 401(k) plans (assuming the money wasn’t already spent). For those that had gone on a buying binge, they were under water and moving to file for bankruptcy. Easy come, easy go!

Leslie Renshaw, Cerent’s human resources manager echoes Bob’s concerns, “This sudden wealth damaged more people than it helped. Marriages fell apart; if people were engaged they broke it off. They’d tell me, ‘I’ve got money and now I can find someone better.’ I would say it had a net damaging effect.”

In spite of advice meted out by Cisco’s human resources department, most engineers paid little heed to the merits of securing financial advice and instead, as Leslie recalls, “They went out and bought cars and jewelry and furs. Their lives were seriously changed because of these spending sprees and not for the best. Then you watched the Cisco stock price go from somewhere around $80 [to $12] at some point and all the people that had left their money only in Cisco stock were effectively ruined.”

In 1999, many people in the middle class made this mistake and invested in the equity markets exclusively; Cerent’s engineers included. They were overconfident that Wall Street’s big returns in a bull market that had existed since 1982 would continue well into the new millennium. During this eighteen-year period, the Dow experienced its most spectacular rise, although with a “minor blip” in 1987. From a low of 777 in August 1982, the index grew more than 1,500 percent to close at almost 11,723 by January 2000. Then the bear market arrived, which lasted until 2003. The index weaved and bobbed at first, like an ocean buoy, and then plunged nearly 40 percent, to a low of 7,286 in October 2002.

But the technology sector and Cisco’s stock price in particular had a far rougher ride and with it the engineers who kept everything or most of their paper wealth invested in Cisco after December 1999. Cisco’s stock price peaked in March 2000 at just over $80 per share and in nine months it lost more than half its value to around $39 per share. The stock took another 100 percent hit in less than three months, reaching a further low of just over $20 per share. Between March and September 2001, another halving of the stock price took place, with shares settling to a low under $12 share.

Anyone making a million dollars from vesting in or buying more Cisco stock saw their money effectively cut in half on three different occasions over an eighteen-month period. This turn of events left newly-minted Cisco millionaires with $125,000, a number that is found in numerous middle-aged, middle-class couples’ combined 401(k) plans (assuming the money wasn’t already spent). For those that had gone on a buying binge, they were under water and moving to file for bankruptcy. Easy come, easy go!

Leslie Renshaw, Cerent’s human resources manager echoes Bob’s concerns, “This sudden wealth damaged more people than it helped. Marriages fell apart; if people were engaged they broke it off. They’d tell me, ‘I’ve got money and now I can find someone better.’ I would say it had a net damaging effect.”

In spite of advice meted out by Cisco’s human resources department, most engineers paid little heed to the merits of securing financial advice and instead, as Leslie recalls, “They went out and bought cars and jewelry and furs. Their lives were seriously changed because of these spending sprees and not for the best. Then you watched the Cisco stock price go from somewhere around $80 [to $12] at some point and all the people that had left their money only in Cisco stock were effectively ruined.”

Bob and Leslie had the experience to avoid financial ruin but some of their colleagues did not pay heed to their warnings about the importance of diversifying and seeking financial advice. Images courtesy Ajaib Bhadare; collage by R.K. Koslowsky.

However, those that hung on to their investment portfolios during this rough time, did well. Those that had diversified beyond simply holding Cisco stock or even investing in all equities did even better.

In the subsequent recession after the dot.com bust and telecom crash, a similar lesson was learned by individual investors. As The Wall Street Journal reported in the fall 2014, “Imagine two households each with $100,000 in the stock market in 2007. A family that sold in 2009 after losing half its portfolio’s value may now have $50,000 in a savings account. A family that held on would now have about $130,000 in stocks. The inequality has dawned merely because of the investing decisions [of two different families].” In just two years, the savings disparity became almost 300 percent.

The Wall Street Journal added, “One unfortunate effect of recessions and stock-market declines is they often induce people to exit the market at exactly the wrong time,” said Dean Maki, chief U.S. economist at Barclays and a former Fed researcher on consumer balance sheets. “In retrospect, anyway, the right thing to do would have been to buy more equities at the trough, not to sell equities at the trough.”

As one financial advisor succinctly summarized the situation, for individual investors, “Timeless wisdom: Fear and greed.” Those that exit the market quickly are the fearful and those that jump in rapidly are the greedy.

The messages for the small investors continue to be diversification, controlled personal spending, and never panic. The latter point is reinforced by recent research conducted by the Federal Reserve and the University of Michigan which reveals that panic about the market widens wealth inequality between those that react and those that stay the course.

The bottom line: Be careful of too much wealth too soon. If you are fortunate to secure wealth, don’t spend it all at once. Save most for a rainy day.

In the subsequent recession after the dot.com bust and telecom crash, a similar lesson was learned by individual investors. As The Wall Street Journal reported in the fall 2014, “Imagine two households each with $100,000 in the stock market in 2007. A family that sold in 2009 after losing half its portfolio’s value may now have $50,000 in a savings account. A family that held on would now have about $130,000 in stocks. The inequality has dawned merely because of the investing decisions [of two different families].” In just two years, the savings disparity became almost 300 percent.

The Wall Street Journal added, “One unfortunate effect of recessions and stock-market declines is they often induce people to exit the market at exactly the wrong time,” said Dean Maki, chief U.S. economist at Barclays and a former Fed researcher on consumer balance sheets. “In retrospect, anyway, the right thing to do would have been to buy more equities at the trough, not to sell equities at the trough.”

As one financial advisor succinctly summarized the situation, for individual investors, “Timeless wisdom: Fear and greed.” Those that exit the market quickly are the fearful and those that jump in rapidly are the greedy.

The messages for the small investors continue to be diversification, controlled personal spending, and never panic. The latter point is reinforced by recent research conducted by the Federal Reserve and the University of Michigan which reveals that panic about the market widens wealth inequality between those that react and those that stay the course.

The bottom line: Be careful of too much wealth too soon. If you are fortunate to secure wealth, don’t spend it all at once. Save most for a rainy day.

RSS Feed

RSS Feed