In a recent BLOG post, we pointed out that Cisco’s acquisition frenzy was stopped cold by 2001. Once favorable external factors became unfriendly as the concurrent dot.com bust and telecom meltdown led to a precipitous drop in business.

The rapid downturn forced John Chambers’ management team to make their “first time ever” cuts in its direct payroll. Over a two-year period, almost 4,000 full-time employees were released [1]. Particularly shocking about this layoff was the fact that Cisco’s full-time (or core) employees were apparently NOT totally insulated by scores of temporary workers that should’ve taken the brunt of the firings.

The rapid downturn forced John Chambers’ management team to make their “first time ever” cuts in its direct payroll. Over a two-year period, almost 4,000 full-time employees were released [1]. Particularly shocking about this layoff was the fact that Cisco’s full-time (or core) employees were apparently NOT totally insulated by scores of temporary workers that should’ve taken the brunt of the firings.

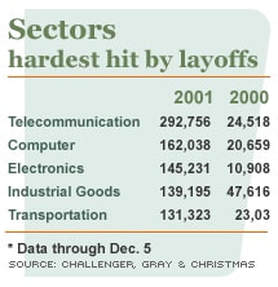

The telecommunications sector was hardest hit with layoffs in 2001; more than a quarter million jobs were pruned from companies’ payrolls. The associated computer and electronics sectors were also severely impacted.

The telecommunications sector was hardest hit with layoffs in 2001; more than a quarter million jobs were pruned from companies’ payrolls. The associated computer and electronics sectors were also severely impacted.

The downturn was so massive in its scope that it reached the very heart of the Cisco faithful. An InfoEdge case study revealed that in Cisco’s manufacturing team employed only one full-time employee for every six part-time workers. While the numbers reveal that “only” ten percent of Cisco employees were severely impacted, the part time ranks supporting the Internet giant were decimated.

The downturn was so massive in its scope that it reached the very heart of the Cisco faithful. An InfoEdge case study revealed that in Cisco’s manufacturing team employed only one full-time employee for every six part-time workers. While the numbers reveal that “only” ten percent of Cisco employees were severely impacted, the part time ranks supporting the Internet giant were decimated.

Cisco’s Troubles But a Symptom of the Telecom Flu of 2001

Companies took the opportunity to slash investments, made during the acquisition-and-develop boom of the late 1990s, that hadn’t borne fruit. These included Ciena’s $474 million purchase of Omnia in July 1999 [2] and Redback’s $4.3 billion acquisition of Siara in March 2000.

Ciena had already made the decision to shutter its newly acquired EdgeDirector product line from Omnia. It was based on ATM technology, which just wasn’t where the industry was headed, especially after service providers began to adopt Ethernet/IP solutions in the access segment. The industry downturn sealed the fate of ATM as a technology solution and froze out ATM-based products like those from Omnia.

Redback’s stock price fell to a 52-week low at $3.85 on August 28, 2001, down from a 52-week high of $171.13 just under a year before, on September 29, 2000. The company was hoping to shake things up and restore its good fortunes by hiring former Cisco executive Kevin DeNuccio [4], who joined Redback on August 29th.

And then 9/11 Eve – Cisco’s Reorganization

Fiber Optic News (FON) reported on the recent Cisco reorganization, just one day before 9/11. Speculation was rampant in the fall of 2001 that Carl Russo, Cisco group vice president of optical networking, “may be on his way out either voluntarily or involuntarily.” FON added, “Given the chance to respond to that scenario, Cisco spokeswoman Jill Martin said the company will not comment on rumors and speculation . . . Russo previously reported to [the recently departed Kevin] Kennedy, and now reports to Jayshree Ullal.”

Cisco sought to reinvent itself as the layoffs began in 2001. The company’s reworked engineering organization was structured into eleven new technology groups, with its marketing effort concentrating on describing Cisco’s technology differentiation to the marketplace.

FON sought the advice of Wall Street analyst and ten-year telecom follower Ariane Mahler of Dresdner Kleinwort Wasserstein. She didn’t think Cisco’s reorganization would ignite much business, arguing, “They are trying to reinvent themselves. They had this big reorganization announcement which I don’t think is really much of an announcement at all.” Continuing to be brutally candid, Mahler adds, “They weren’t doing well in the service provider market, and with this reorganization, I think they have even less of a chance in that market.”

Cerent Success Debated

Contrary to Jayshree Ullal’s view that Cerent was an overwhelming success for Cisco (from the vantage point of 2013 hindsight), in late 2001, Doug Green, previously an executive with Chromatis, pointed out that many acquisitions, including his own by Lucent, were a flop, as described above. FON reported on Green’s feelings on September 10, 2001, “Even acquisitions that seem to be strong, such as Cisco’s $6.9 billion acquisition of Cerent in Aug. 1999, might not be quite what they seem . . . If you look at that [Cerent] product, they paid almost $7 billion for it, and they probably brought in $2 billion of revenue.”

Doug Green concludes, “Even though that’s a great success story [3], has it really paid off in terms of return on investment? I don’t know that anybody did a great job of M&A over the last two years. People were just thinking they had to get in the game and were flying blindly in most cases.”

Then 9/11

I suspect no one read the above referenced telecom stories on September 11th of 2001. The world was shocked as the people of the United States experienced a horrific terror attack. One of Cisco’s own, Suzanne Calley, was killed by suicidal jihadists. She was a passenger on the doomed American Airlines flight 77; a flight that targeted and then struck part of the Pentagon.

Companies took the opportunity to slash investments, made during the acquisition-and-develop boom of the late 1990s, that hadn’t borne fruit. These included Ciena’s $474 million purchase of Omnia in July 1999 [2] and Redback’s $4.3 billion acquisition of Siara in March 2000.

Ciena had already made the decision to shutter its newly acquired EdgeDirector product line from Omnia. It was based on ATM technology, which just wasn’t where the industry was headed, especially after service providers began to adopt Ethernet/IP solutions in the access segment. The industry downturn sealed the fate of ATM as a technology solution and froze out ATM-based products like those from Omnia.

Redback’s stock price fell to a 52-week low at $3.85 on August 28, 2001, down from a 52-week high of $171.13 just under a year before, on September 29, 2000. The company was hoping to shake things up and restore its good fortunes by hiring former Cisco executive Kevin DeNuccio [4], who joined Redback on August 29th.

And then 9/11 Eve – Cisco’s Reorganization

Fiber Optic News (FON) reported on the recent Cisco reorganization, just one day before 9/11. Speculation was rampant in the fall of 2001 that Carl Russo, Cisco group vice president of optical networking, “may be on his way out either voluntarily or involuntarily.” FON added, “Given the chance to respond to that scenario, Cisco spokeswoman Jill Martin said the company will not comment on rumors and speculation . . . Russo previously reported to [the recently departed Kevin] Kennedy, and now reports to Jayshree Ullal.”

Cisco sought to reinvent itself as the layoffs began in 2001. The company’s reworked engineering organization was structured into eleven new technology groups, with its marketing effort concentrating on describing Cisco’s technology differentiation to the marketplace.

FON sought the advice of Wall Street analyst and ten-year telecom follower Ariane Mahler of Dresdner Kleinwort Wasserstein. She didn’t think Cisco’s reorganization would ignite much business, arguing, “They are trying to reinvent themselves. They had this big reorganization announcement which I don’t think is really much of an announcement at all.” Continuing to be brutally candid, Mahler adds, “They weren’t doing well in the service provider market, and with this reorganization, I think they have even less of a chance in that market.”

Cerent Success Debated

Contrary to Jayshree Ullal’s view that Cerent was an overwhelming success for Cisco (from the vantage point of 2013 hindsight), in late 2001, Doug Green, previously an executive with Chromatis, pointed out that many acquisitions, including his own by Lucent, were a flop, as described above. FON reported on Green’s feelings on September 10, 2001, “Even acquisitions that seem to be strong, such as Cisco’s $6.9 billion acquisition of Cerent in Aug. 1999, might not be quite what they seem . . . If you look at that [Cerent] product, they paid almost $7 billion for it, and they probably brought in $2 billion of revenue.”

Doug Green concludes, “Even though that’s a great success story [3], has it really paid off in terms of return on investment? I don’t know that anybody did a great job of M&A over the last two years. People were just thinking they had to get in the game and were flying blindly in most cases.”

Then 9/11

I suspect no one read the above referenced telecom stories on September 11th of 2001. The world was shocked as the people of the United States experienced a horrific terror attack. One of Cisco’s own, Suzanne Calley, was killed by suicidal jihadists. She was a passenger on the doomed American Airlines flight 77; a flight that targeted and then struck part of the Pentagon.

AA 77 struck the Pentagon. Here, first responders are dousing the flames. Image courtesy FBI.

Recovery and Redemption in Cisco’s FY2002

“The year 2002 marked an uptick in Cisco optical,” I wrote in 2015, “in spite of the economic downturn felt by the disastrous economic effects of the dot.com bust and the telecom meltdown. Cisco weathered the initial storm reasonably well with strong financial results posted for the quarterly period ending April 27, 2002 with a GAAP net income of $729 million, up almost 11 percent from the previous quarter. Cisco remained in the black for its fiscal year 2002, leaving it a “relative wealth in resources to compete against financially troubled competitors like Lucent and Nortel.”

[1] The full-time employee rolls dropped from 38,402 employees down to 34,446 during 2001 and 2002. The 3,956 released employees represented ten percent of Cisco’s total headcount.

[2] On the same day in March 1999 that Ciena acquired Lightera, its most successful pick-up, Ciena also acquired Marlborough, Massachusetts-based Omnia for another, almost half-a-billion dollars. This carrier-class multi-service access platform did not fair well in the marketplace. It, and its product contributions, were omitted from Ciena’s glossy brochure recounting the history of the company.

[3] Kevin DeNuccio, my boss’s boss starting in late 1999, spent six years at Cisco, where he served as senior vice president of worldwide service provider operations. As chief salesman, he likely left as sales at Cisco all but evaporated during Cisco’s fiscal year 2001.

[4] Certainly not as charitable as Jayshree in hindsight, Doug from a 2001 perspective may have been internalizing sour grapes as first, his technology bet on metropolitan WDM with Chromatis, and second, its subsequent acquisition by Lucent crashed and burned. How could he not say that Cerent was success with a billion dollar run rate in sales? “As it turned out,” I wrote in a previous BLOG post, “Chromatis had misread the optical transport market on a number of fronts: Metro DWDM was not the fast-growing segment, hundreds of millions of dollars in the sales pipeline was a myth, and Metro DWDM did not offer a cost-effective alternative to next generation SONET. On top of that, Lucent reached a point where it’s business downturn forced the company to prune its product mix and focus on the needs of its thirty largest customers. Chromatis bit the dust in August 2001, after just being acquired in May 2000 – a $4.5 billion mistake.”

“The year 2002 marked an uptick in Cisco optical,” I wrote in 2015, “in spite of the economic downturn felt by the disastrous economic effects of the dot.com bust and the telecom meltdown. Cisco weathered the initial storm reasonably well with strong financial results posted for the quarterly period ending April 27, 2002 with a GAAP net income of $729 million, up almost 11 percent from the previous quarter. Cisco remained in the black for its fiscal year 2002, leaving it a “relative wealth in resources to compete against financially troubled competitors like Lucent and Nortel.”

[1] The full-time employee rolls dropped from 38,402 employees down to 34,446 during 2001 and 2002. The 3,956 released employees represented ten percent of Cisco’s total headcount.

[2] On the same day in March 1999 that Ciena acquired Lightera, its most successful pick-up, Ciena also acquired Marlborough, Massachusetts-based Omnia for another, almost half-a-billion dollars. This carrier-class multi-service access platform did not fair well in the marketplace. It, and its product contributions, were omitted from Ciena’s glossy brochure recounting the history of the company.

[3] Kevin DeNuccio, my boss’s boss starting in late 1999, spent six years at Cisco, where he served as senior vice president of worldwide service provider operations. As chief salesman, he likely left as sales at Cisco all but evaporated during Cisco’s fiscal year 2001.

[4] Certainly not as charitable as Jayshree in hindsight, Doug from a 2001 perspective may have been internalizing sour grapes as first, his technology bet on metropolitan WDM with Chromatis, and second, its subsequent acquisition by Lucent crashed and burned. How could he not say that Cerent was success with a billion dollar run rate in sales? “As it turned out,” I wrote in a previous BLOG post, “Chromatis had misread the optical transport market on a number of fronts: Metro DWDM was not the fast-growing segment, hundreds of millions of dollars in the sales pipeline was a myth, and Metro DWDM did not offer a cost-effective alternative to next generation SONET. On top of that, Lucent reached a point where it’s business downturn forced the company to prune its product mix and focus on the needs of its thirty largest customers. Chromatis bit the dust in August 2001, after just being acquired in May 2000 – a $4.5 billion mistake.”

RSS Feed

RSS Feed