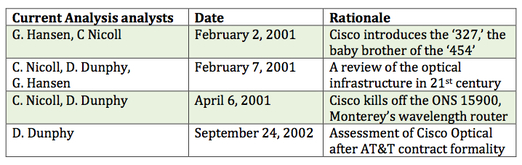

Current Analysis, an east coast industry research firm, came out in early 2001 and late 2002 with a number of reports centered on the nation’s optical infrastructure and Cisco’s emerging role in the optical transport space.

Their February 2001 report, “Cisco’s New ONS 15327, Downsized 15454 or Chevy Engine?” was “positive on Cisco’s introduction of the ONS 15327 aimed at metropolitan access applications.” This firm of industry analysts viewed the baby brother of the ‘454’ as having a very high market impact. The even smaller ‘327’ package from Cisco brought “the technology of the highly successful ONS 15454 SONET platform to the access markets . . .”

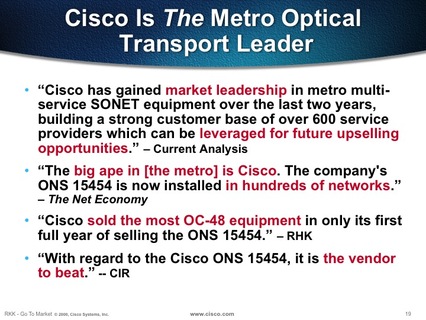

Current Analysis cautioned the legacy SONET vendors of Cisco’s expanding optical portfolio, “Competitors will have to respond strongly to Cisco’s ability to leverage its base of over 500 customers for the parent product.” Current Analysis outlined the challenges for companies like Nortel and Lucent, “Competitors have their hands full with the new systems from Redback [Siara Systems, one of the two Fiberlane splinters] and Cisco [Cerent Corp., the other Fiberlane splinter]. Nortel is the market leader in the access platform market, but the 3500 is due for an update to both shrink physical size as well as needing to add a more access focused feature set, including [electrical cross-connect] functionality . . . The 3-[rack unit] height of the 15327 offering allows it to go places [Nortel’s] OPtera products can’t.”

With integrated Ethernet functionality on the ONS 15327, Current Analysis points out that “the emphasis is changing from transport delivery to service delivery,” a point that Scott Messenger and I discussed in part 10 of my book The Upstart Startup.

With integrated Ethernet functionality on the ONS 15327, Current Analysis points out that “the emphasis is changing from transport delivery to service delivery,” a point that Scott Messenger and I discussed in part 10 of my book The Upstart Startup.

Operationally, Cisco’s ONS 15000-family eliminated the need for “manual provisioning of circuits across SONET rings,” which from legacy SONET equipment vendors had “slow[ed] provisioning time and increase[d] the opportunity for mistakes.” In a message directed at the large Baby Bells, Current Analysis wrote, “Service Providers have started to embrace newer solutions that address technology and service requirements and also operational issues.”

Changes in society and how both consumers and business wanted to conduct business in the early 2000s drove the need for service providers to change and move to new optical platforms that could embrace e-commerce. Current Analysis observed, “The continued socialization of the Internet as a business and personal information source presages the ongoing growth of Internet access. The needs for ubiquitous access, extended access (beyond home PCs to include consumer goods and wireless communications), and high-speed access are the social drivers impacting the optical transmission vendors.”

Companies like Nortel and Lucent were being forced to innovate and startups were thriving in a highly funded optical environment pushing for new heights in innovation. Optical networks delivered the required capacity for the sprawling Internet and delivered a low delay, high quality signal for transporting all manner of traffic, be it voice, data, or video.

Current Analysis reiterated this last point, “Consumers now expect more out of their online experience and are taking advantage of voice, video, sound, and motion. Shoppers expect to see what they are looking to buy from various angles (if not from all angles) and in a multiplicity of colors. [E-commerce] vendors are responding with sites that deliver what the user wants.”

Fourteen years later, these capabilities are table stakes for all good retail websites, regardless of how they are accessed.

While the ‘327’ introduction protected Cisco’s optical sales momentum of the ‘454’ on the low end of the transport market, the ‘900’ product born of the Monterey acquisition was ineffective at protecting the market-leading ‘454’ on the high end. Furthermore, Cisco became impatient with the slow growth of the relatively small optical switching market in 2001. Current Analysis and other industry analysts agreed with Cisco pulling the plug on the ongoing development of Monterey’s wavelength router – the Cisco ONS 15900. Chris Nicoll and Dave Dunphy wrote, “Cisco discontinues a troubled product that was diverting development resources, had obvious problems, and attracted significant criticism. Moving on to more productive enterprises and eliminating the target of criticism will allow Cisco to focus attention back on its viable projects and current success in the metro.”

Even if Cisco had stayed the course, the company would have had a lot of ground to make up against Ciena’s system, the CoreDirector, that made strong inroads in the switching market “due to its STS-1 granularity,” and ability to support optical switching in the future, Cisco also would have encountered fierce competition from Sycamore and its optical switching product, the SN 16000.

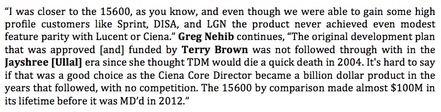

Greg Nehib, who came from the Monterey acquisition and has remained at Cisco for the past 15 years, told me, “The 15900 was cancelled after Cisco missed AT&T's lab entry date. AT&T ultimately told the 15900 team that they lost their spot in the lab. I know the AT&T guys expected Cisco to ‘double down’ and beg forgiveness, but like you stated, it was a tough market and an easy project to bail on under the circumstances.”

Indeed, the company decided to focus on its metro network dominance and, as Current Analysis presciently notes, “Cisco should consider a platform that replaces the SONET ADM/[switching] functionality on a scale larger than what can be addressed by the ONS 15454.” Cisco was already doing that. The company abandoned the ONS 15900 and put most of the Dallas-based Monterey team on a switching platform based on the ‘454’ architecture.

Greg recalls, “Most of the 15900 [development] team came onto the 15600 project immediately. Only about 20 percent of the former 15900 staff went to augment ‘454’ development efforts.”

Shortly thereafter, Cisco introduced the ONS 15600 as a ‘454’ on steroids with massive electrical switching capability. But that product was too late to the market to make significant inroads. This product supported Cisco’s IP + Optical and intelligent optical network push and filled the gaping hole left by the termination of the ONS 15900 optical switching product, but it never met with significant customer acceptance. Cisco ruled the MAN but could not effectively crack the WAN unless it funded end-to-end infrastructure products through its finance group – Cisco, like Lucent and Nortel, effectively started to buy its own equipment for service providers such as El Paso and others.

Another weak optical contributor at the time was Cisco’s Pirelli acquisition that brought long-haul equipment to Cisco’s ONS portfolio. The ONS 15800 family could not stand up to a Nortel, Lucent, or Ciena long-haul optical transport system and this fact left analysts unsatisfied with Cisco’s total optical portfolio, “Cisco does not have the same level of expertise in long-haul WAN solutions as it does in the MAN; the Pirelli system has been very slow in gaining market acceptance, and the failure of the 15900 further illustrates this problem.”

While this was true on a systems level, it was not true at the component level. To this day, Cisco has retained its Monza, Italy group for optical innovation and assisting the company’s business development group with further optical acquisitions to ensure continued organic growth in the service provider segment.

In spite of the AT&T cancellation of a $25 million order for the Monterey product that Cisco eventually abandoned, this Tier 1 service provider saw the merits of Cisco’s optical portfolio. The ONS 15454 as well as Cisco’s CTM management platform were being used across AT&T’s metro networks in volume by February 2002.

In an ironic twist, the ‘454s’ at AT&T would interface with Ciena’s CoreDirector electrical switching platform, a product from Lightera, a company that Carl Russo had wanted to acquire before Ciena did. In fact, Carl beforehand had designs on acquiring Ciena when it could have been vulnerable for acquisition in late 1998. It was the strength of the CoreDirector that doomed the Monterey product in AT&T and the marketplace at large. By the same token, it was the strength of the Cerent product that doomed Ciena’s MetroDirector K2 product that it had acquired from Cyras, a startup company that had copied Cerent’s offering by 2000. So, both Cisco and Ciena survived, but their Monterey and Cyras acquisitions died, in large part, due to the decisions made by AT&T.

Changes in society and how both consumers and business wanted to conduct business in the early 2000s drove the need for service providers to change and move to new optical platforms that could embrace e-commerce. Current Analysis observed, “The continued socialization of the Internet as a business and personal information source presages the ongoing growth of Internet access. The needs for ubiquitous access, extended access (beyond home PCs to include consumer goods and wireless communications), and high-speed access are the social drivers impacting the optical transmission vendors.”

Companies like Nortel and Lucent were being forced to innovate and startups were thriving in a highly funded optical environment pushing for new heights in innovation. Optical networks delivered the required capacity for the sprawling Internet and delivered a low delay, high quality signal for transporting all manner of traffic, be it voice, data, or video.

Current Analysis reiterated this last point, “Consumers now expect more out of their online experience and are taking advantage of voice, video, sound, and motion. Shoppers expect to see what they are looking to buy from various angles (if not from all angles) and in a multiplicity of colors. [E-commerce] vendors are responding with sites that deliver what the user wants.”

Fourteen years later, these capabilities are table stakes for all good retail websites, regardless of how they are accessed.

While the ‘327’ introduction protected Cisco’s optical sales momentum of the ‘454’ on the low end of the transport market, the ‘900’ product born of the Monterey acquisition was ineffective at protecting the market-leading ‘454’ on the high end. Furthermore, Cisco became impatient with the slow growth of the relatively small optical switching market in 2001. Current Analysis and other industry analysts agreed with Cisco pulling the plug on the ongoing development of Monterey’s wavelength router – the Cisco ONS 15900. Chris Nicoll and Dave Dunphy wrote, “Cisco discontinues a troubled product that was diverting development resources, had obvious problems, and attracted significant criticism. Moving on to more productive enterprises and eliminating the target of criticism will allow Cisco to focus attention back on its viable projects and current success in the metro.”

Even if Cisco had stayed the course, the company would have had a lot of ground to make up against Ciena’s system, the CoreDirector, that made strong inroads in the switching market “due to its STS-1 granularity,” and ability to support optical switching in the future, Cisco also would have encountered fierce competition from Sycamore and its optical switching product, the SN 16000.

Greg Nehib, who came from the Monterey acquisition and has remained at Cisco for the past 15 years, told me, “The 15900 was cancelled after Cisco missed AT&T's lab entry date. AT&T ultimately told the 15900 team that they lost their spot in the lab. I know the AT&T guys expected Cisco to ‘double down’ and beg forgiveness, but like you stated, it was a tough market and an easy project to bail on under the circumstances.”

Indeed, the company decided to focus on its metro network dominance and, as Current Analysis presciently notes, “Cisco should consider a platform that replaces the SONET ADM/[switching] functionality on a scale larger than what can be addressed by the ONS 15454.” Cisco was already doing that. The company abandoned the ONS 15900 and put most of the Dallas-based Monterey team on a switching platform based on the ‘454’ architecture.

Greg recalls, “Most of the 15900 [development] team came onto the 15600 project immediately. Only about 20 percent of the former 15900 staff went to augment ‘454’ development efforts.”

Shortly thereafter, Cisco introduced the ONS 15600 as a ‘454’ on steroids with massive electrical switching capability. But that product was too late to the market to make significant inroads. This product supported Cisco’s IP + Optical and intelligent optical network push and filled the gaping hole left by the termination of the ONS 15900 optical switching product, but it never met with significant customer acceptance. Cisco ruled the MAN but could not effectively crack the WAN unless it funded end-to-end infrastructure products through its finance group – Cisco, like Lucent and Nortel, effectively started to buy its own equipment for service providers such as El Paso and others.

Another weak optical contributor at the time was Cisco’s Pirelli acquisition that brought long-haul equipment to Cisco’s ONS portfolio. The ONS 15800 family could not stand up to a Nortel, Lucent, or Ciena long-haul optical transport system and this fact left analysts unsatisfied with Cisco’s total optical portfolio, “Cisco does not have the same level of expertise in long-haul WAN solutions as it does in the MAN; the Pirelli system has been very slow in gaining market acceptance, and the failure of the 15900 further illustrates this problem.”

While this was true on a systems level, it was not true at the component level. To this day, Cisco has retained its Monza, Italy group for optical innovation and assisting the company’s business development group with further optical acquisitions to ensure continued organic growth in the service provider segment.

In spite of the AT&T cancellation of a $25 million order for the Monterey product that Cisco eventually abandoned, this Tier 1 service provider saw the merits of Cisco’s optical portfolio. The ONS 15454 as well as Cisco’s CTM management platform were being used across AT&T’s metro networks in volume by February 2002.

In an ironic twist, the ‘454s’ at AT&T would interface with Ciena’s CoreDirector electrical switching platform, a product from Lightera, a company that Carl Russo had wanted to acquire before Ciena did. In fact, Carl beforehand had designs on acquiring Ciena when it could have been vulnerable for acquisition in late 1998. It was the strength of the CoreDirector that doomed the Monterey product in AT&T and the marketplace at large. By the same token, it was the strength of the Cerent product that doomed Ciena’s MetroDirector K2 product that it had acquired from Cyras, a startup company that had copied Cerent’s offering by 2000. So, both Cisco and Ciena survived, but their Monterey and Cyras acquisitions died, in large part, due to the decisions made by AT&T.

To parlay Cisco’s strength in optical metro markets by 2002, I worked with Jayshree Ullal and the various business units across Cisco to introduce a cohesive marketing message surrounding end-to-end optical networking. We marketed Cisco’s metro optical networking solutions under the name COMET for Complete Optical Multiservice Edge and Transport.

The year 2002 marked an uptake in Cisco optical, in spite of the economic downturn felt by the disastrous economic effects of the dot.com bust and the telecom meltdown. Cisco weathered the initial storm reasonably well with strong financial results posted for the quarterly period ending April 27, 2002 with a GAAP net income of $729 million, up almost 11 percent from the previous quarter. Cisco remained in the black for its fiscal year 2002, leaving it a “relative wealth in resources to compete against financially troubled competitors like Lucent and Nortel.”

Cisco’s COMET messaging compelled analysts like Current Analysis to view Cisco’s optical portfolio in a positive light, “We are taking a slightly positive stance on Cisco. Solid entry into the metro optical transport markets with its multiservice SONET systems (the ONS 15454 and later the ONS 15327) and metro DWDM (the ONS 15200 [from Qeyton systems]) was accompanied by less that expected results from the acquisitions that were intended to gain strong long-haul switching (i.e., Monterey) and transport (i.e, Pirelli). The loss of the 15900 left a bit of a hole in Cisco’s IP + Optical strategy, but the new 15600 is better targeted toward current carrier needs [with electrical switching instead of optical switching] and builds a stronger metro [solution].”

Cisco went on to nurture the Cerent DNA it had acquired and develop carrier class products that would target service providers for years to come. In fact, Cisco introduced a carrier class operating system for its routers such as the CRS-1 – IOSXR for service provider customers – in the years that followed. Not only that, but the 15600 chassis and system architecture, built upon ‘454’ concepts, according to Greg Nehib, “was considered for re-use in the platforms that are now the ASR 9000 and the new NCS 4000, due to its split backplane and the ability to route [and] switch multiple traffic types.”

The year 2002 marked an uptake in Cisco optical, in spite of the economic downturn felt by the disastrous economic effects of the dot.com bust and the telecom meltdown. Cisco weathered the initial storm reasonably well with strong financial results posted for the quarterly period ending April 27, 2002 with a GAAP net income of $729 million, up almost 11 percent from the previous quarter. Cisco remained in the black for its fiscal year 2002, leaving it a “relative wealth in resources to compete against financially troubled competitors like Lucent and Nortel.”

Cisco’s COMET messaging compelled analysts like Current Analysis to view Cisco’s optical portfolio in a positive light, “We are taking a slightly positive stance on Cisco. Solid entry into the metro optical transport markets with its multiservice SONET systems (the ONS 15454 and later the ONS 15327) and metro DWDM (the ONS 15200 [from Qeyton systems]) was accompanied by less that expected results from the acquisitions that were intended to gain strong long-haul switching (i.e., Monterey) and transport (i.e, Pirelli). The loss of the 15900 left a bit of a hole in Cisco’s IP + Optical strategy, but the new 15600 is better targeted toward current carrier needs [with electrical switching instead of optical switching] and builds a stronger metro [solution].”

Cisco went on to nurture the Cerent DNA it had acquired and develop carrier class products that would target service providers for years to come. In fact, Cisco introduced a carrier class operating system for its routers such as the CRS-1 – IOSXR for service provider customers – in the years that followed. Not only that, but the 15600 chassis and system architecture, built upon ‘454’ concepts, according to Greg Nehib, “was considered for re-use in the platforms that are now the ASR 9000 and the new NCS 4000, due to its split backplane and the ability to route [and] switch multiple traffic types.”

RSS Feed

RSS Feed