In the late 1990s, the dot.com bubble era witnessed the introduction of new metrics by fledgling startups to indicate financial strength: growth in “eyeballs,” increase in website visits, and a slew of other non-GAAP terms [1]. In a recent BLOG, I noted that profitability was replaced by growth during the late 1990s and this trend has reappeared today.

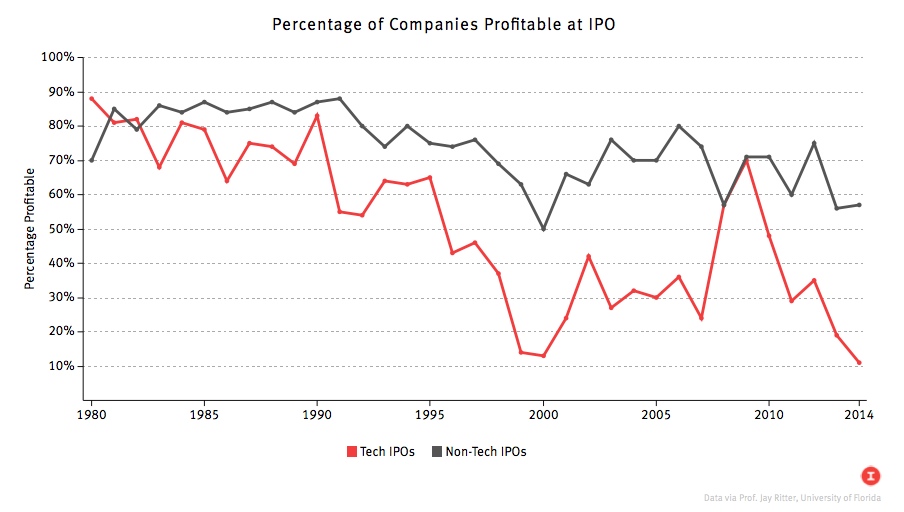

I wrote, “University of Florida Professor Jay Ritter, recently reported that in 1999 and 2000 only 14 and 13 percent of technology company IPOs, respectively, were profitable, down from the pre-dot.com era of 1996 and 1997, when 43 and 46 percent of them, respectively, were profitable . . . Jay cautions that a similar situation is appearing today with only 11 percent of the technology IPOs from 2014 operating at a profit, a level even below the 13 percent of 2000.”

I wrote, “University of Florida Professor Jay Ritter, recently reported that in 1999 and 2000 only 14 and 13 percent of technology company IPOs, respectively, were profitable, down from the pre-dot.com era of 1996 and 1997, when 43 and 46 percent of them, respectively, were profitable . . . Jay cautions that a similar situation is appearing today with only 11 percent of the technology IPOs from 2014 operating at a profit, a level even below the 13 percent of 2000.”

In 1999 and 2000 only 14 and 13 percent of technology company IPOs, respectively, were profitable. Data for image courtesy Jay Ritter.

It’s important for early stage investors to ask questions about the source of a company’s declared revenue. In fact, other metrics may be substituted for revenue by some privately-held companies: bookings, billings, annual recurring revenues, and more. Their objective is to project “positive” views of their company’s financials with numbers that exceed actual revenue.

Back in the days prior to the telecom meltdown, a number of optical startups touted favorable progress by highlighting the number of lab and field trials underway, for example, all for no revenue. This “trial” equipment was given to prospective customers to “sample the dog food,” to see if it was palatable for their network.

In today’s software-intensive startup environment, free software is provided to try out a product or service. Then positive reviews are given to investors and/or stockholders for the number of hits (site visits), the number of likes, and so on. With such metrics being used, the performance of the company appears to be solid. Skeptics, including most accountants, believe that entrepreneurs in the tech sector are too confident with their marketing and actually set up the company for failure. While I understand this point, the very essence of an entrepreneur and the mindset of a startup organization is confidence, not to the point of cockiness or hubris, but in the belief that their solution to a market need is the right one.

I suppose the counterpoint to this perceived over-confidence is the investors, who should not go along with creative financial terms to represent company progress. In this way, inflated valuations can be minimized and headroom may be left for any missteps in a startup’s early life. Of course, astronomical valuations can lead to massive IPOs or huge acquisition prices.

At $6.9 billion, one could argue that the Cerent valuation recognized by Cisco in late 1999 was astronomical. The question remains, “Did Cisco receive value for its purchase price of Cerent?”

[1] In September 2015, in order to test this assertion, eight startups representing a diverse industry set – transportation, refrigeration, software product, services, pharmaceutical, retail, and building materials – presented at a recent event in Sonoma County. Several of these startups were pre-revenue, others had already produced prototypes and generating revenue, and some were already manufacturing product and simply needed funds for expansion. This group of eight could also be categorized as either high-tech or low-tech. Regardless, they all presented metrics that played to their advantage. These included the quality of their board of directors, the quality of strategic partnerships forged, their role as a disruptor in the chosen sector, the pedigree of the leadership team, a track history of winning prizes at startup contests, their unique “solution” to the “problem” as they defined it, and the size of their addressable market. Those startups that were up and running cited the more traditional metrics over the “new age” metrics. Revenue growth, the size of the customer base, the number of units sold, and strategies adopted to reduce cost of sales were mentioned more than web activity and social media marketing.

Back in the days prior to the telecom meltdown, a number of optical startups touted favorable progress by highlighting the number of lab and field trials underway, for example, all for no revenue. This “trial” equipment was given to prospective customers to “sample the dog food,” to see if it was palatable for their network.

In today’s software-intensive startup environment, free software is provided to try out a product or service. Then positive reviews are given to investors and/or stockholders for the number of hits (site visits), the number of likes, and so on. With such metrics being used, the performance of the company appears to be solid. Skeptics, including most accountants, believe that entrepreneurs in the tech sector are too confident with their marketing and actually set up the company for failure. While I understand this point, the very essence of an entrepreneur and the mindset of a startup organization is confidence, not to the point of cockiness or hubris, but in the belief that their solution to a market need is the right one.

I suppose the counterpoint to this perceived over-confidence is the investors, who should not go along with creative financial terms to represent company progress. In this way, inflated valuations can be minimized and headroom may be left for any missteps in a startup’s early life. Of course, astronomical valuations can lead to massive IPOs or huge acquisition prices.

At $6.9 billion, one could argue that the Cerent valuation recognized by Cisco in late 1999 was astronomical. The question remains, “Did Cisco receive value for its purchase price of Cerent?”

[1] In September 2015, in order to test this assertion, eight startups representing a diverse industry set – transportation, refrigeration, software product, services, pharmaceutical, retail, and building materials – presented at a recent event in Sonoma County. Several of these startups were pre-revenue, others had already produced prototypes and generating revenue, and some were already manufacturing product and simply needed funds for expansion. This group of eight could also be categorized as either high-tech or low-tech. Regardless, they all presented metrics that played to their advantage. These included the quality of their board of directors, the quality of strategic partnerships forged, their role as a disruptor in the chosen sector, the pedigree of the leadership team, a track history of winning prizes at startup contests, their unique “solution” to the “problem” as they defined it, and the size of their addressable market. Those startups that were up and running cited the more traditional metrics over the “new age” metrics. Revenue growth, the size of the customer base, the number of units sold, and strategies adopted to reduce cost of sales were mentioned more than web activity and social media marketing.

RSS Feed

RSS Feed