“Fortune knocks but once, but misfortune has much more patience.”

– Laurence J. Peter (1919–1990)

– Laurence J. Peter (1919–1990)

Cisco, almost from the start, operated as an “arbitrage-oriented firm.”

Such firms, as described by Barry Lynn in his book, End of the Line: The Rise and Coming Fall of the Global Corporation (2005), “are designed to focus much more on using their power over their production systems to wring out wealth immediately, rather than to devote resources to technologies that might create wealth years from now.”

The emphasis placed on “production systems” is mine. In an earlier BLOG post, I reviewed how Cisco leveraged outsourcing to bring its manufacturing costs way down. For example, “By 2000, some 90 percent of Cisco’s subassembly work took place outside the company, as Cisco managers kept control only of high-end, developmental production work.”

Cisco and other firms of this bent viewed “development of new technologies and new products, rather than an investment in the future, as no more than an unnecessary and probably unwise cost.”

A Frenzied Acquisition Force

And it was this inane philosophy that drove Cisco to its acquisition and develop (A&D) mindset instead of the more traditional research and development (R&D) approach used by competitors such as Nortel, Lucent, and Tellabs.

During the 1990s, many entrepreneurs in and around Silicon Valley, including Ed Paulson, who, in his book, Inside Cisco (2001), began to refer to Cisco “as the ‘borg,’ [1] owing to the company’s ‘innovation through acquisition strategy.’ Between mid-1993 and mid-2001, Cisco purchased 71 firms in one of the most extravagant buying sprees in high-tech history.”

Cisco collected engineering talent and new products with a speed that astounded industry observers and Wall Street denizens alike. The company knew, as Lynn reported, “that success lay in moving very fast to capture control of its marketplace. And in part, the strategy emerged simply because the company could afford to do so.”

As the price of the Internet giant’s stock soared, “Cisco’s top managers found themselves atop a vast pool of ‘capital’ for acquisition,” and they wasted no time in using that value to ramp up its buying spree in 1998.

Such firms, as described by Barry Lynn in his book, End of the Line: The Rise and Coming Fall of the Global Corporation (2005), “are designed to focus much more on using their power over their production systems to wring out wealth immediately, rather than to devote resources to technologies that might create wealth years from now.”

The emphasis placed on “production systems” is mine. In an earlier BLOG post, I reviewed how Cisco leveraged outsourcing to bring its manufacturing costs way down. For example, “By 2000, some 90 percent of Cisco’s subassembly work took place outside the company, as Cisco managers kept control only of high-end, developmental production work.”

Cisco and other firms of this bent viewed “development of new technologies and new products, rather than an investment in the future, as no more than an unnecessary and probably unwise cost.”

A Frenzied Acquisition Force

And it was this inane philosophy that drove Cisco to its acquisition and develop (A&D) mindset instead of the more traditional research and development (R&D) approach used by competitors such as Nortel, Lucent, and Tellabs.

During the 1990s, many entrepreneurs in and around Silicon Valley, including Ed Paulson, who, in his book, Inside Cisco (2001), began to refer to Cisco “as the ‘borg,’ [1] owing to the company’s ‘innovation through acquisition strategy.’ Between mid-1993 and mid-2001, Cisco purchased 71 firms in one of the most extravagant buying sprees in high-tech history.”

Cisco collected engineering talent and new products with a speed that astounded industry observers and Wall Street denizens alike. The company knew, as Lynn reported, “that success lay in moving very fast to capture control of its marketplace. And in part, the strategy emerged simply because the company could afford to do so.”

As the price of the Internet giant’s stock soared, “Cisco’s top managers found themselves atop a vast pool of ‘capital’ for acquisition,” and they wasted no time in using that value to ramp up its buying spree in 1998.

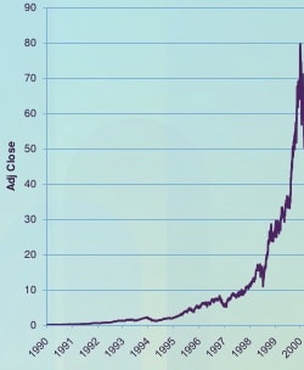

Cisco’s stock rose to about $80 early in the new millennium. Graphic courtesy Cisco.

Cisco’s strategy was simplicity itself. Customers shared their needs and the company would buy the required technologies to satisfy those needs. Cisco adapted to emerging technologies as close to instantaneous as any company could. One could argue that Cisco was tuned to the market just like a venture capitalist firm. And the company was able to ride the wave of technological fads.

For instance, Cisco’s investment in Ethernet switching was a big success.

Their subsequent investment in ATM turned out to be a bust in the long-term, but it allowed them a Trojan horse filled with IP/Ethernet-solutions to infiltrate the service provider marketplace.

However, the company fared much better in optical investments. Cerent was the standout in optical transport, but the other five of the six company investments in optical products were a bust [2]. However, the good news here is that the engineering talent that remained from the other acquired optical companies helped to rapidly evolve the Cerent 454 (now the Cisco ONS 15454) platform and make Cisco a major optical competitor.

Innovation through New Technology Introduction

“Viewed from an innovation system perspective,” writes Lynn, Cisco’s strategy during the 1990s helped “to maintain Cisco as the keystone predator within a venture capital ecosystem. Indeed, Cisco . . . fostered what became an entirely new model for identifying, incubating, and introducing new technologies. Small firms supported by venture capital took the hard initial steps and incurred the initial risks. In exchange, Cisco provided the ‘exit,’ rewarding founders and funders at the small companies with rich chunks of Cisco stock and sometimes lucrative jobs inside the firm.”

Upstart startups planted the seeds and tended their saplings, while Cisco harvested the ripest fruit. This process delivered a bumper crop through early 2001, but then, the market leader succumbed to a myriad of events that tell the other half of the story, best illustrated by the graphic below.

For instance, Cisco’s investment in Ethernet switching was a big success.

Their subsequent investment in ATM turned out to be a bust in the long-term, but it allowed them a Trojan horse filled with IP/Ethernet-solutions to infiltrate the service provider marketplace.

However, the company fared much better in optical investments. Cerent was the standout in optical transport, but the other five of the six company investments in optical products were a bust [2]. However, the good news here is that the engineering talent that remained from the other acquired optical companies helped to rapidly evolve the Cerent 454 (now the Cisco ONS 15454) platform and make Cisco a major optical competitor.

Innovation through New Technology Introduction

“Viewed from an innovation system perspective,” writes Lynn, Cisco’s strategy during the 1990s helped “to maintain Cisco as the keystone predator within a venture capital ecosystem. Indeed, Cisco . . . fostered what became an entirely new model for identifying, incubating, and introducing new technologies. Small firms supported by venture capital took the hard initial steps and incurred the initial risks. In exchange, Cisco provided the ‘exit,’ rewarding founders and funders at the small companies with rich chunks of Cisco stock and sometimes lucrative jobs inside the firm.”

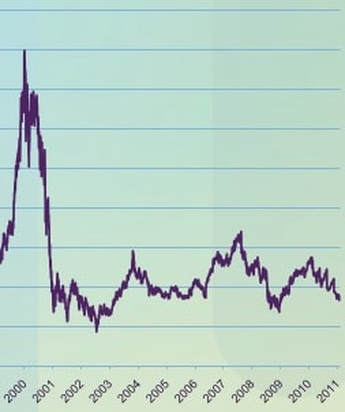

Upstart startups planted the seeds and tended their saplings, while Cisco harvested the ripest fruit. This process delivered a bumper crop through early 2001, but then, the market leader succumbed to a myriad of events that tell the other half of the story, best illustrated by the graphic below.

Cisco’s stock fell like a rock from its $80 highs in early 2001 to a level that settled around $15 by 2011. Graphic courtesy Cisco.

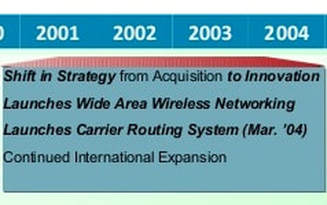

Cisco acknowledged it was out of the frenzied acquisition game with, in part, a 2005 presentation it posted on its website. Graphic excerpt courtesy Cisco.

Cisco acknowledged it was out of the frenzied acquisition game with, in part, a 2005 presentation it posted on its website. Graphic excerpt courtesy Cisco. In response to these challenging times, Cisco shed both employees and product lines. The company surrendered its acquisition-and-develop model and silently telegraphed this shift in strategy as the telecom meltdown reached its height. By 2005, Cisco acknowledged its curtailment of frenzied acquisitions in most of the company’s presentations, in favor of in-house “innovation,” something that it had sporadically done in the past.

The question today, “Is this shift in strategy working?” And does this “mature company” approach allow Cisco to achieve growth and higher stock valuations like it once knew?

Its shareholders still want to know.

[1] In the Star Trek universe, the “Borg” annex the technology and knowledge of other alien species to the Collective by forcibly assimilating them, and in the process transforming individual beings into drones. The Borg's ultimate goal is to achieve perfection.

[2] The other five optical acquisitions included Monterey (1), acquired on the same day as Cerent, in 1999, for its optical cross-connect technology. Pirelli (2), and Qeyton Systems (3) and their WDM-centric products turned out to be a bust in terms of generating revenue. Other optically-oriented resources shoehorned into the optical business unit from other failed acquisitions such as Pipelinks (4) and Fibex (5) had to be redeployed from a management perspective. For example, research scientists out of Monza, Italy from the Pirelli acquisition were able to add value to the acquired Cerent product line, but this occurred years later. For the company as a whole, Cisco doubled its revenue from $19 billion in 2000 to $38 billion in 2013. Cerent’s one billion dollar contribution was more than five percent of Cisco’s 2000 total revenue metric, almost all of which bolstered the company’s service provider segment. Read chapter 9 of The Upstart Startup for more.

Its shareholders still want to know.

[1] In the Star Trek universe, the “Borg” annex the technology and knowledge of other alien species to the Collective by forcibly assimilating them, and in the process transforming individual beings into drones. The Borg's ultimate goal is to achieve perfection.

[2] The other five optical acquisitions included Monterey (1), acquired on the same day as Cerent, in 1999, for its optical cross-connect technology. Pirelli (2), and Qeyton Systems (3) and their WDM-centric products turned out to be a bust in terms of generating revenue. Other optically-oriented resources shoehorned into the optical business unit from other failed acquisitions such as Pipelinks (4) and Fibex (5) had to be redeployed from a management perspective. For example, research scientists out of Monza, Italy from the Pirelli acquisition were able to add value to the acquired Cerent product line, but this occurred years later. For the company as a whole, Cisco doubled its revenue from $19 billion in 2000 to $38 billion in 2013. Cerent’s one billion dollar contribution was more than five percent of Cisco’s 2000 total revenue metric, almost all of which bolstered the company’s service provider segment. Read chapter 9 of The Upstart Startup for more.

RSS Feed

RSS Feed