If ever there was a wayward startup and an acquiring company caught up in the frenzy of paying billions for startups, they were collectively known as Xros (pronounced KAI-ros) and Nortel Networks, respectively.

Nortel paid an incredible $3.25 billion for Xros in 2000 [1], after Xros announced its X-1000 product at the Optical Fiber Conference (OFC) in March of that year.

Lessons can be learned from this deal by venture capitalists, and acquiring companies alike, about when to acquire, although even the most diligent of established companies can be seduced by the hype of a startups’ concept. To wit, Cisco was swayed by the potential of an idea, when it acquired Monterey Networks, in August 1999, for its optical cross-connect product sporting mirrors – Micro Electro-Mechanical Systems (MEMS) to be precise.

Nortel secured Xros and its 90 employees without a finished MEMS-based product and the apparent inability to pronounce the company’s name (and less than a year after Cisco’s Monterey acquisition). “But [Xros] had generated massive hype at the Optical Fiber Conference in Baltimore,” as Fiber Optics News reported on March 11, 2000, “with its demo of a high-capacity optical cross-connect system for open optical networks.”

Rajiv Ramaswami, vice-president, system architecture, of Xros, based in Sunnyvale, California [2], advocated for this all-optical micro-mirror switch technology “to shift the paths of wavelengths” (as George Gilder liked to describe it). Like Monterey’s Wavelength Router, which was cut from the same cloth, Xros never sold one, and the product was quietly retired by Nortel. Cisco’s competing optical cross-connect (re-named the ONS-15900) continued development inside Cisco until it was quickly relegated to the scrap heap of engineering ideas arriving too soon to market. AT&T had cancelled its order for the ONS-15900, providing Cisco with an overwhelming reason to abort its short-lived optical switching program. Having no customers and gaining little market acceptance tend to kill even the most exciting technological ideas. Nortel seemed not to have gotten the memo.

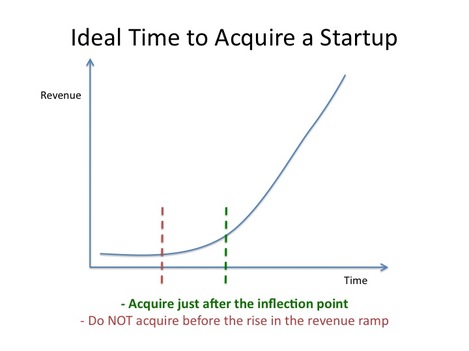

A simplistic view of when it’s time to acquire a startup, as shown below, should have caused Nortel to stay clear of its Xros acquisition in the first place. There was simply no revenue stream to justify this startup’s valuation, let alone the multi-billion dollar acquisition cost.

Nortel paid an incredible $3.25 billion for Xros in 2000 [1], after Xros announced its X-1000 product at the Optical Fiber Conference (OFC) in March of that year.

Lessons can be learned from this deal by venture capitalists, and acquiring companies alike, about when to acquire, although even the most diligent of established companies can be seduced by the hype of a startups’ concept. To wit, Cisco was swayed by the potential of an idea, when it acquired Monterey Networks, in August 1999, for its optical cross-connect product sporting mirrors – Micro Electro-Mechanical Systems (MEMS) to be precise.

Nortel secured Xros and its 90 employees without a finished MEMS-based product and the apparent inability to pronounce the company’s name (and less than a year after Cisco’s Monterey acquisition). “But [Xros] had generated massive hype at the Optical Fiber Conference in Baltimore,” as Fiber Optics News reported on March 11, 2000, “with its demo of a high-capacity optical cross-connect system for open optical networks.”

Rajiv Ramaswami, vice-president, system architecture, of Xros, based in Sunnyvale, California [2], advocated for this all-optical micro-mirror switch technology “to shift the paths of wavelengths” (as George Gilder liked to describe it). Like Monterey’s Wavelength Router, which was cut from the same cloth, Xros never sold one, and the product was quietly retired by Nortel. Cisco’s competing optical cross-connect (re-named the ONS-15900) continued development inside Cisco until it was quickly relegated to the scrap heap of engineering ideas arriving too soon to market. AT&T had cancelled its order for the ONS-15900, providing Cisco with an overwhelming reason to abort its short-lived optical switching program. Having no customers and gaining little market acceptance tend to kill even the most exciting technological ideas. Nortel seemed not to have gotten the memo.

A simplistic view of when it’s time to acquire a startup, as shown below, should have caused Nortel to stay clear of its Xros acquisition in the first place. There was simply no revenue stream to justify this startup’s valuation, let alone the multi-billion dollar acquisition cost.

Graphic courtesy R.K. Koslowsky

In hindsight, former Cisco executives Tom Fallon and Jayshree Ullal (who hailed from the Crescendo acquisition) viewed Cerent as a model acquisition. It was the best way to acquire and integrate a company in order to preserve its autonomy and maintain its momentum in the marketplace. By 1999, Cisco had become the ‘seasoned veteran’ at successfully acquiring and integrating startup companies

Tom Fallon, now Infinera’s CEO, provides further evidence on exactly when to buy a technology company, “Cerent was a good example. Cisco bought a lot of companies that were at the technology stage. Some of those didn’t work so well. They bought a lot of companies that were at the big revenue stage. Some of those didn’t work so well either. Cerent, to me, was the model, and we talked about that at Cisco, of when to buy a company. It’s after the technology is proven. It’s after initial traction in the market, but before the explosive growth and adoption and Cisco could accelerate that explosive growth and adoption. And Cerent was a good proof point of this.”

An example of what not to do is to acquire a company before it has proven its technology with customers. Tom cites the premature acquisition Nortel made of its optical cross-connect startup, “Xros was valued at four billion dollars and they never went to market.”

Nortel’s seduction was total, failing to achieve a happy ending, and never receiving a customer order. The Xros science experiment (which formed the guts of the Nortel OPTera ConnectPX) entered customer trials, but it never saw the light of an installed customer network. This optical cross-connect failed to appear during Nortel’s announced “end of 2001” availability window. Fiber Optics News (FON) wrote, “Nortel’s HDX solution meets customer needs better than the PX.”

It took Nortel two years to recognize their blunder. They worded this failure, in March 2002, by saying the company “would postpone indefinitely the market debut of this large-scale switch that incorporated the Xros technology.”

Xros had already quietly disappeared. A low-level Nortel spokesman shared the obvious conclusion with FON in 2002, “. . . stand-alone photonic switches are likely to be longer-term market requirements.”

Indeed, service providers were interested in reducing capital expenditures and cutting operational expenses, as the Cerent team recognized in 1998. Optical transport customers were not focused on large-scale, stand-alone systems. Nortel found a scapegoat for their acquisition folly and blamed the telecom meltdown for their misstep, “The dramatic changes in market conditions have changed the key customer value proposition from a focus on scale to a focus on capex/opex reduction . . . It has become clear that optical spending will now focus on interconnect and bandwidth management, as well as operational challenges.”

Lesson learned. Due diligence, not hype, should define when to acquire a startup.

[1] “Between 1996 and 2001,” according to Om Malik, in his book Broadbandits (2004), “venture capitalists spent $8.7 billion in different sorts of broadband-related technologies, including optical (invested). During the same time, Cisco, Lucent, and Nortel spent $105 billion on acquisitions,” [more than 12-times that of the VC community] . . . “After Cisco’s $6.9 billion price tag [for Cerent], an all-time high, the value of acquisitions started to decline: Siara at $4.3 billion, Chromatis (Lucent) at $4.5 billion, Xros (Nortel) at $3.2 billion, Qtera (Nortel) at $3 billion, Cyras (Ciena) at $2.3 billion.”

[2] Rajiv Ramaswami left Tellabs in 1999 after leading a team for two years trying to develop a metropolitan optical transport product. He came up against fierce competition in the form of Cerent in 1998. Bit by the startup bug, Rajiv joined Xros, parlaying his Tellabs cross-connect experience. Then, Nortel quickly snapped up Xros in 2000 and Rajiv became a Nortel employee working on open optical system architectures. He left Nortel in 2002 once the Xros product was shuttered. And, in an ironic twist, he joined his former competitor, Cisco with its optical networking group, that year. Jayshree Ullal hired Rajiv. She put him to work rationalizing the DWDM evolution for the optical team, and this led to the split of the ‘454’ program into the MSPP (SONET) and MSTP (DWDM) developments. He held various roles at Cisco for a number of years until ending up at Broadcom. With his involvement, Tellabs lost the race to Cerent in the late 1990s to build a metro optical transport product, and then Nortel (with Xros) lost the race to Ciena in the early 2000s to build an optical cross-connect offering. But the evolution and the success of Cerent’s original ‘454’ continued with his support. If you can’t beat them, join them. [Information pulled from Rajiv’s Linkedin profile, August 2016.]

Nortel’s seduction was total, failing to achieve a happy ending, and never receiving a customer order. The Xros science experiment (which formed the guts of the Nortel OPTera ConnectPX) entered customer trials, but it never saw the light of an installed customer network. This optical cross-connect failed to appear during Nortel’s announced “end of 2001” availability window. Fiber Optics News (FON) wrote, “Nortel’s HDX solution meets customer needs better than the PX.”

It took Nortel two years to recognize their blunder. They worded this failure, in March 2002, by saying the company “would postpone indefinitely the market debut of this large-scale switch that incorporated the Xros technology.”

Xros had already quietly disappeared. A low-level Nortel spokesman shared the obvious conclusion with FON in 2002, “. . . stand-alone photonic switches are likely to be longer-term market requirements.”

Indeed, service providers were interested in reducing capital expenditures and cutting operational expenses, as the Cerent team recognized in 1998. Optical transport customers were not focused on large-scale, stand-alone systems. Nortel found a scapegoat for their acquisition folly and blamed the telecom meltdown for their misstep, “The dramatic changes in market conditions have changed the key customer value proposition from a focus on scale to a focus on capex/opex reduction . . . It has become clear that optical spending will now focus on interconnect and bandwidth management, as well as operational challenges.”

Lesson learned. Due diligence, not hype, should define when to acquire a startup.

[1] “Between 1996 and 2001,” according to Om Malik, in his book Broadbandits (2004), “venture capitalists spent $8.7 billion in different sorts of broadband-related technologies, including optical (invested). During the same time, Cisco, Lucent, and Nortel spent $105 billion on acquisitions,” [more than 12-times that of the VC community] . . . “After Cisco’s $6.9 billion price tag [for Cerent], an all-time high, the value of acquisitions started to decline: Siara at $4.3 billion, Chromatis (Lucent) at $4.5 billion, Xros (Nortel) at $3.2 billion, Qtera (Nortel) at $3 billion, Cyras (Ciena) at $2.3 billion.”

[2] Rajiv Ramaswami left Tellabs in 1999 after leading a team for two years trying to develop a metropolitan optical transport product. He came up against fierce competition in the form of Cerent in 1998. Bit by the startup bug, Rajiv joined Xros, parlaying his Tellabs cross-connect experience. Then, Nortel quickly snapped up Xros in 2000 and Rajiv became a Nortel employee working on open optical system architectures. He left Nortel in 2002 once the Xros product was shuttered. And, in an ironic twist, he joined his former competitor, Cisco with its optical networking group, that year. Jayshree Ullal hired Rajiv. She put him to work rationalizing the DWDM evolution for the optical team, and this led to the split of the ‘454’ program into the MSPP (SONET) and MSTP (DWDM) developments. He held various roles at Cisco for a number of years until ending up at Broadcom. With his involvement, Tellabs lost the race to Cerent in the late 1990s to build a metro optical transport product, and then Nortel (with Xros) lost the race to Ciena in the early 2000s to build an optical cross-connect offering. But the evolution and the success of Cerent’s original ‘454’ continued with his support. If you can’t beat them, join them. [Information pulled from Rajiv’s Linkedin profile, August 2016.]

RSS Feed

RSS Feed