“I am concerned about losing our ability to experiment, disrupt the status quo, innovate and rebel.”

- Hossein Moiin, Nokia Networks, circa 2015 on innovation

- Hossein Moiin, Nokia Networks, circa 2015 on innovation

Venture capitalists and entrepreneurs are crazy!

They want to change the world.

And many of these innovators tried to introduce change during the late 1990s, fueled by the rise of the Internet in an environment of deregulation. Change was rapidly embraced in the telecommunications sector, especially in the optical transport space, an area that “went beserk” with venture capital thrown at it.

Let’s look at some of those crazy ideas that appeared between 1997 and 1999!

Cerent’s idea and that upstart startup’s early success, in hindsight, seemed to be downright sane. The company solved a problem for service providers that needed more cost-effective transport of voice and data traffic across metropolitan networks. That was it.

The company’s cofounders asked, “Why not produce a product at 1/3 the cost that consumed half the space and power of competing products that could operate in all of the popular configurations with more useful features and a simple user interface?”

Indeed. In less than three years on the market, the company shipped $1 billion worth of Cerent 454s.

Such success inspired copycats. The optical transport market was big and growing. But not all of the crazy ideas were good. Some were bad and others were ugly. If nothing else, Cerent’s alumni should be flattered that so many others tried to crack the metropolitan optical transport market with their own crazy ideas.

The Copycats

Copycat products from companies imitating Cerent began to appear from the likes of Redback (using the Siara Systems engineering team that came from the other half of the Fiberlane splinter), Metro-Optix, and White Rock; to the data-centric boxes like those from Alidian and Chromatis; to the wavelength-centric boxes like those from Kestrel, ONI and Sycamore, all of which, except for Sycamore, never found sustained traction.

They want to change the world.

And many of these innovators tried to introduce change during the late 1990s, fueled by the rise of the Internet in an environment of deregulation. Change was rapidly embraced in the telecommunications sector, especially in the optical transport space, an area that “went beserk” with venture capital thrown at it.

Let’s look at some of those crazy ideas that appeared between 1997 and 1999!

Cerent’s idea and that upstart startup’s early success, in hindsight, seemed to be downright sane. The company solved a problem for service providers that needed more cost-effective transport of voice and data traffic across metropolitan networks. That was it.

The company’s cofounders asked, “Why not produce a product at 1/3 the cost that consumed half the space and power of competing products that could operate in all of the popular configurations with more useful features and a simple user interface?”

Indeed. In less than three years on the market, the company shipped $1 billion worth of Cerent 454s.

Such success inspired copycats. The optical transport market was big and growing. But not all of the crazy ideas were good. Some were bad and others were ugly. If nothing else, Cerent’s alumni should be flattered that so many others tried to crack the metropolitan optical transport market with their own crazy ideas.

The Copycats

Copycat products from companies imitating Cerent began to appear from the likes of Redback (using the Siara Systems engineering team that came from the other half of the Fiberlane splinter), Metro-Optix, and White Rock; to the data-centric boxes like those from Alidian and Chromatis; to the wavelength-centric boxes like those from Kestrel, ONI and Sycamore, all of which, except for Sycamore, never found sustained traction.

While many of these startups failed, both Cerent and Siara, derived from Raj Singh and Vinod Khosla’s Fiberlane, became part of Cisco and Redback, respectively, through acquisition. Other optical transport startups that went public after 2000 were not so well insulated from the slowdown in capital spending of the dot.com bust and telecom meltdown or the muted challenge to established service providers from competitive carriers.

These troubling trends began to appear in 2001, reducing the revenue projections of many of them. Their built-in cost structure and continued high cash burn rates made these copycats unable to tolerate the time it would take to travel the much longer road to profitability. Any service provider capital to be spent was more likely to find its way to established vendors, such as Cisco, instead of startups, especially those new companies with untested products that had yet to be evaluated. The pretenders who tried to ride the coat tails of Cerent came in three types [1].

First, there were the blatant copycats including Redback (Siara Systems), Metro-Optix, and White Rock, all which eventually failed in the marketplace.

Second, there were those data-centric boxes like those from Alidian and Chromatis that failed in the marketplace, primarily because they couldn’t easily accommodate voice traffic.

Third, wavelength-centric boxes like those from Kestrel, ONI and Sycamore never found sustained traction. One could argue that delivering “a wavelength to every desktop” was way ahead of the usefulness curve, although Sycamore’s “all-optical” focus brought some good success in the long haul market for over a decade.

What Did Customers Think About Cerent’s Crazy Idea?

Wayne Price, CTO of Williams Communications, summed it best in 1999, when he saw how easy the Cerent 454 was to install in the company’s Tulsa, Oklahoma lab, “I see a lot of slideshows from a lot of companies, and I get a little skeptical about the claim these startups make. But Cerent was different. They shipped us their box within a few days, without sending an engineer to baby-sit. My lab guys were able to get it hooked up in two hours. That’s an unheard of scenario in this business.”

Brad Lester of US West recalls, “There were a lot of products that came and went during that time period, including ones from Movaz, Mahi, Turin [2], Corvis, and Chromatis.” But none of them were soon enough and none could do what the Cerent 454 did in 2000. Brad adds, “The 454 was a hard act to follow in 2000 and it fit the U S West needs better at the time.”

There is a lot of value in being first to market, especially if you get it right by talking to early adopter customers at the outset.

U S West ultimately selected the Cerent 454 as its second inter-office facilities (IOF) solution. Fujitsu had been the main SONET product for IOF until Cerent came along and took at least half of this business away. Brad believes U S West played a crucial role in shaping the Cerent 454, all of which later made the product palatable to other Bell companies such as SBC and BellSouth.

Forget the copycats. There’s nothing like an original, and the Cerent 454 was just that!

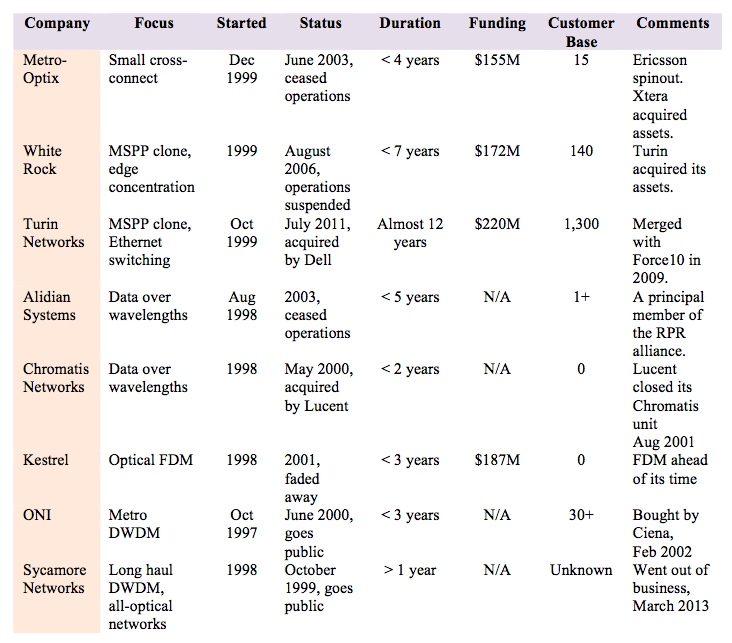

[1] The following table summarizes the brave efforts of many entrepreneurs to crack the metropolitan transport market in the late 1990s and early 2000s. Only a few product ideas left a lasting legacy.

These troubling trends began to appear in 2001, reducing the revenue projections of many of them. Their built-in cost structure and continued high cash burn rates made these copycats unable to tolerate the time it would take to travel the much longer road to profitability. Any service provider capital to be spent was more likely to find its way to established vendors, such as Cisco, instead of startups, especially those new companies with untested products that had yet to be evaluated. The pretenders who tried to ride the coat tails of Cerent came in three types [1].

First, there were the blatant copycats including Redback (Siara Systems), Metro-Optix, and White Rock, all which eventually failed in the marketplace.

Second, there were those data-centric boxes like those from Alidian and Chromatis that failed in the marketplace, primarily because they couldn’t easily accommodate voice traffic.

Third, wavelength-centric boxes like those from Kestrel, ONI and Sycamore never found sustained traction. One could argue that delivering “a wavelength to every desktop” was way ahead of the usefulness curve, although Sycamore’s “all-optical” focus brought some good success in the long haul market for over a decade.

What Did Customers Think About Cerent’s Crazy Idea?

Wayne Price, CTO of Williams Communications, summed it best in 1999, when he saw how easy the Cerent 454 was to install in the company’s Tulsa, Oklahoma lab, “I see a lot of slideshows from a lot of companies, and I get a little skeptical about the claim these startups make. But Cerent was different. They shipped us their box within a few days, without sending an engineer to baby-sit. My lab guys were able to get it hooked up in two hours. That’s an unheard of scenario in this business.”

Brad Lester of US West recalls, “There were a lot of products that came and went during that time period, including ones from Movaz, Mahi, Turin [2], Corvis, and Chromatis.” But none of them were soon enough and none could do what the Cerent 454 did in 2000. Brad adds, “The 454 was a hard act to follow in 2000 and it fit the U S West needs better at the time.”

There is a lot of value in being first to market, especially if you get it right by talking to early adopter customers at the outset.

U S West ultimately selected the Cerent 454 as its second inter-office facilities (IOF) solution. Fujitsu had been the main SONET product for IOF until Cerent came along and took at least half of this business away. Brad believes U S West played a crucial role in shaping the Cerent 454, all of which later made the product palatable to other Bell companies such as SBC and BellSouth.

Forget the copycats. There’s nothing like an original, and the Cerent 454 was just that!

[1] The following table summarizes the brave efforts of many entrepreneurs to crack the metropolitan transport market in the late 1990s and early 2000s. Only a few product ideas left a lasting legacy.

Table courtesy R.K. Koslowsky

[2] One of those startups that did quite well during the 2002 and 2003 downturn was Turin Networks, a company also funded, in part, by Telecom Valley’s Don Green and initially headed by one of his protégé’s and founder John Webley. Turin would continue to build momentum in the MSPP space at Cerent’s, now Cisco’s, expense. After all, competition is healthy for the marketplace.

RSS Feed

RSS Feed