Flaunting the term “super cycle” for the optical technology sector is an attention getter for those seeking to grab viewers and hold them on their web pages.

Image courtesy Maxim Kazmin_Fotolia stock.adobe.com

Recently [1], Therese Poletti, wrote, “Like most component and semiconductor markets, this sector is extremely cyclical—as soon as the first big internet build-out pushed optical- networking companies to outlandish valuations, the cycle ended and they came crashing down amid the massive telecommunications bust.”

Prompted by the thoughts of one financial analyst, Cowen & Company’s Paul Silverstein, Poletti penned a piece on the coming return to the heydays of Internet construction fever and high company valuations.

Hold on. Reporting on a few companies [2] with higher than average growth multiples is not a reason to proclaim the arrival of an optical supercycle at the outset of 2017. Even Silverstein, as bankers are prone to do, hedges his stock pick bets with caution, “Investors are leery of a sector that saw an estimated $1 trillion loss in market value during the dot-com bust.”

Indeed, investors have to enthusiastically drive demand for optical component companies’ stocks [2] and see their chosen portfolio of companies rise in value, quarter after quarter, as did dozens of companies during the late 1990s. This is not happening, and certainly Poletti and Silverstein’s claims cannot be touted as the dawn of a new supercycle just based on one quarter of financial results. Maybe this analysis can be revisited in a year.

Besides, other external factors exist to dampen a potential optical supercycle from happening now. Some of these outside influences include regulatory uncertainty; the shifting of voice, data, and even video to wireless infrastructures; predictable bandwidth demand for the foreseeable future, even as Asian spending softens; and continued lower cost-per-bit offerings rooted in 100G technology.

Prompted by the thoughts of one financial analyst, Cowen & Company’s Paul Silverstein, Poletti penned a piece on the coming return to the heydays of Internet construction fever and high company valuations.

Hold on. Reporting on a few companies [2] with higher than average growth multiples is not a reason to proclaim the arrival of an optical supercycle at the outset of 2017. Even Silverstein, as bankers are prone to do, hedges his stock pick bets with caution, “Investors are leery of a sector that saw an estimated $1 trillion loss in market value during the dot-com bust.”

Indeed, investors have to enthusiastically drive demand for optical component companies’ stocks [2] and see their chosen portfolio of companies rise in value, quarter after quarter, as did dozens of companies during the late 1990s. This is not happening, and certainly Poletti and Silverstein’s claims cannot be touted as the dawn of a new supercycle just based on one quarter of financial results. Maybe this analysis can be revisited in a year.

Besides, other external factors exist to dampen a potential optical supercycle from happening now. Some of these outside influences include regulatory uncertainty; the shifting of voice, data, and even video to wireless infrastructures; predictable bandwidth demand for the foreseeable future, even as Asian spending softens; and continued lower cost-per-bit offerings rooted in 100G technology.

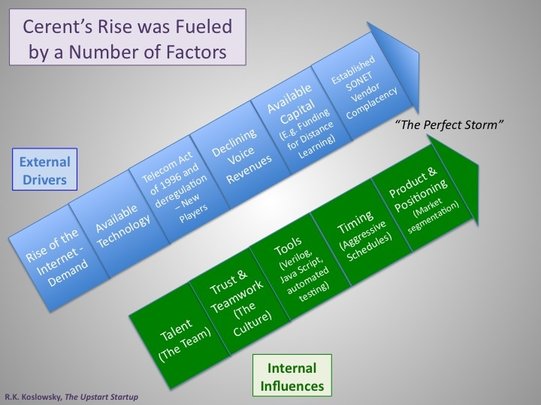

External factors affecting telecom during the late 1990s. Image courtesy R.K. Koslowsky. Taken from his book, The Upstart Startup.

On top of that, established companies such as Cisco Systems continue to downplay the influence of optical networking. That technology has not been mentioned in its quarterly financial results calls or annual reports for years.

After the “terabit tsunami” enthusiasm of the late 1990s, optical hit a brick wall. Cisco even shopped its optical business around (a team dominated by acquired Cerent employees) for a time during the mid-2000s and as one Cisco employee told me after I left the company in 2003, “It wasn't a management shuffle . . . it was a political dismemberment of OTBU [Cisco’s Optical Transport Business Unit] into the DWDM or MSTP portion, which went to the CRBU [Cisco’s Core Routing Business Unit] and the TDM or MSPP portion, which merged with Scientific Atlanta Cable products division.”

If an “optical supercyle” really existed, maybe Cisco’s stock would return to its loftier 80-dollar levels of the early 2000s, accompanied by triple-digit growth.

Mark Lutkowitz, another industry observer agrees with my skeptical assessment, “Obviously, certain analysts on the Street have been pushing the exaggerated characterization for their own purposes, with our favorite that it is ‘a bona fide optical supercycle.’”

Indeed. Optical Supercycle, SCHMOptical Supercycle.

[1] In October 2016, Poletti wrote about the so-called optical supercycle in her article, A dormant tech sector is suddenly surging like it’s 1999. She never replied to my request for more information to substantiate her attention-getting headlines.

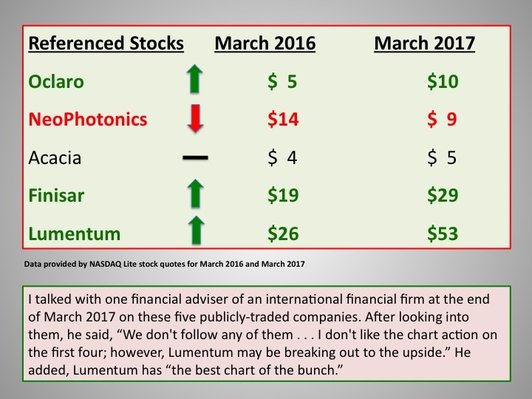

[2] Poletti references only five company stocks in her write-up, and these are not the big optical transport suppliers such as Infinera, Ciena, and Cisco Systems, among other optical systems suppliers:

After the “terabit tsunami” enthusiasm of the late 1990s, optical hit a brick wall. Cisco even shopped its optical business around (a team dominated by acquired Cerent employees) for a time during the mid-2000s and as one Cisco employee told me after I left the company in 2003, “It wasn't a management shuffle . . . it was a political dismemberment of OTBU [Cisco’s Optical Transport Business Unit] into the DWDM or MSTP portion, which went to the CRBU [Cisco’s Core Routing Business Unit] and the TDM or MSPP portion, which merged with Scientific Atlanta Cable products division.”

If an “optical supercyle” really existed, maybe Cisco’s stock would return to its loftier 80-dollar levels of the early 2000s, accompanied by triple-digit growth.

Mark Lutkowitz, another industry observer agrees with my skeptical assessment, “Obviously, certain analysts on the Street have been pushing the exaggerated characterization for their own purposes, with our favorite that it is ‘a bona fide optical supercycle.’”

Indeed. Optical Supercycle, SCHMOptical Supercycle.

[1] In October 2016, Poletti wrote about the so-called optical supercycle in her article, A dormant tech sector is suddenly surging like it’s 1999. She never replied to my request for more information to substantiate her attention-getting headlines.

[2] Poletti references only five company stocks in her write-up, and these are not the big optical transport suppliers such as Infinera, Ciena, and Cisco Systems, among other optical systems suppliers:

Oclaro

NeoPhotonics

Acacia

Finisar

Lumentum

NeoPhotonics

Acacia

Finisar

Lumentum

RSS Feed

RSS Feed